MacroScope Weekly — July 12, 2026

Current Regime: Reflation / Expanding Liquidity

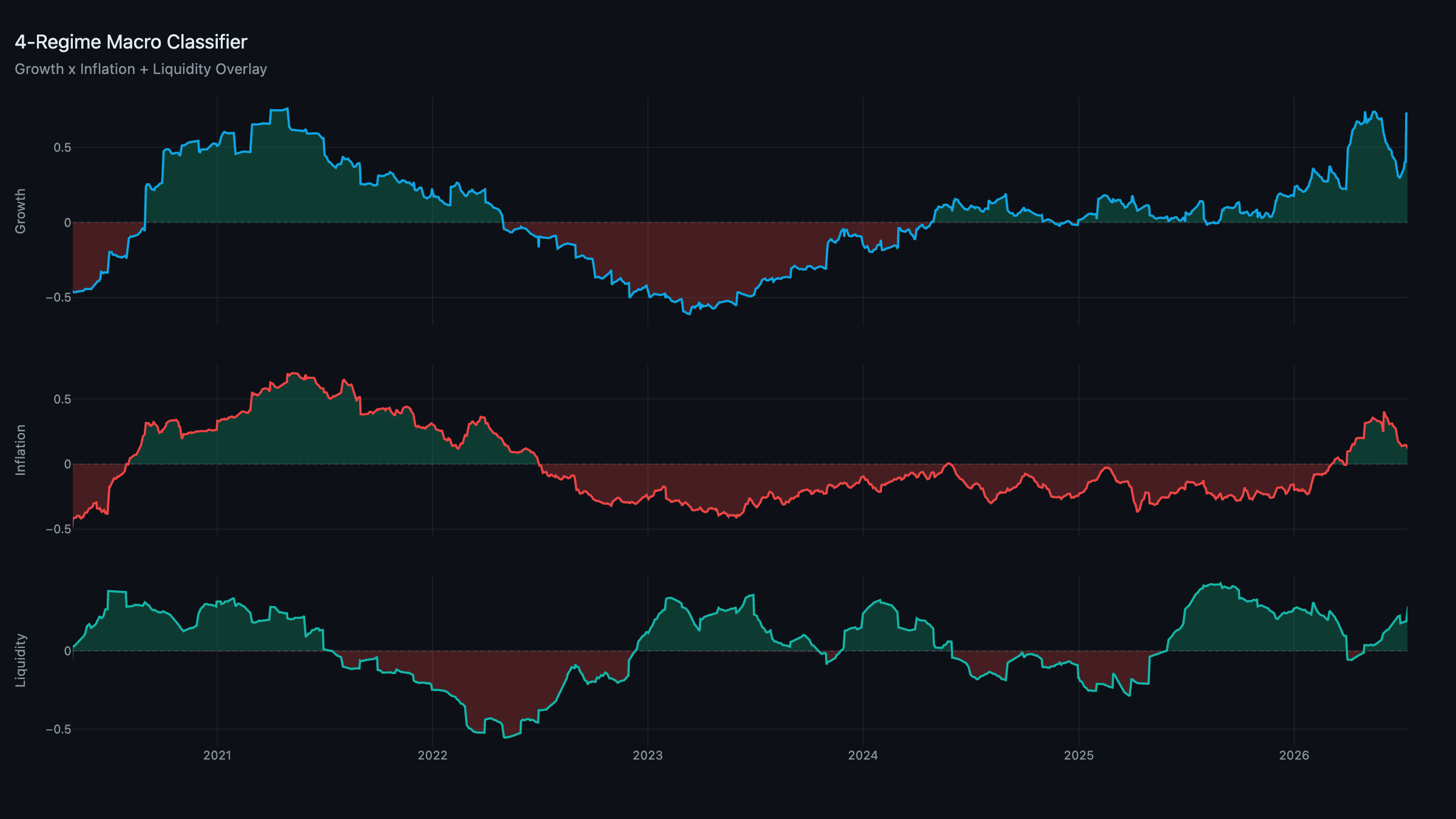

TL;DR: Reflation / Expanding holds, and growth just posted its strongest print of the year at +0.73, up sharply from +0.34 a week ago. Inflation ticked up slightly to +0.14 but remains well off its spring peak, and liquidity firmed to +0.19. The bigger headlines this week were corporate and geopolitical: SpaceX's addition to the Nasdaq-100 puts it directly in QQQ, one of the book's two growth-sleeve holdings, right as sentiment on Elon Musk himself has never been more polarized — and split-screen with that, Iran formally broke off the peace framework it signed just weeks ago, reopening the oil-market tail risk the framework has been watching all year.

Composites: Growth's Best Week of the Year

Growth surged to +0.73, its highest reading since the composite's current form launched — a broad-based print across the production and distribution pillars, not a single-indicator fluke. Inflation edged up to +0.14 from +0.14 the week prior, effectively flat and still far below the spring energy-shock peak; the pipeline-costs channel is the one to watch given the oil move discussed below. Liquidity firmed to +0.19, holding the Expanding state comfortably.

The regime stays Reflation / Expanding, and with growth this strong, the framework's read is unambiguous: this is a cycle firming, not cresting. The one variable that could change that quickly is oil, and that's exactly where the week's biggest geopolitical risk sits.

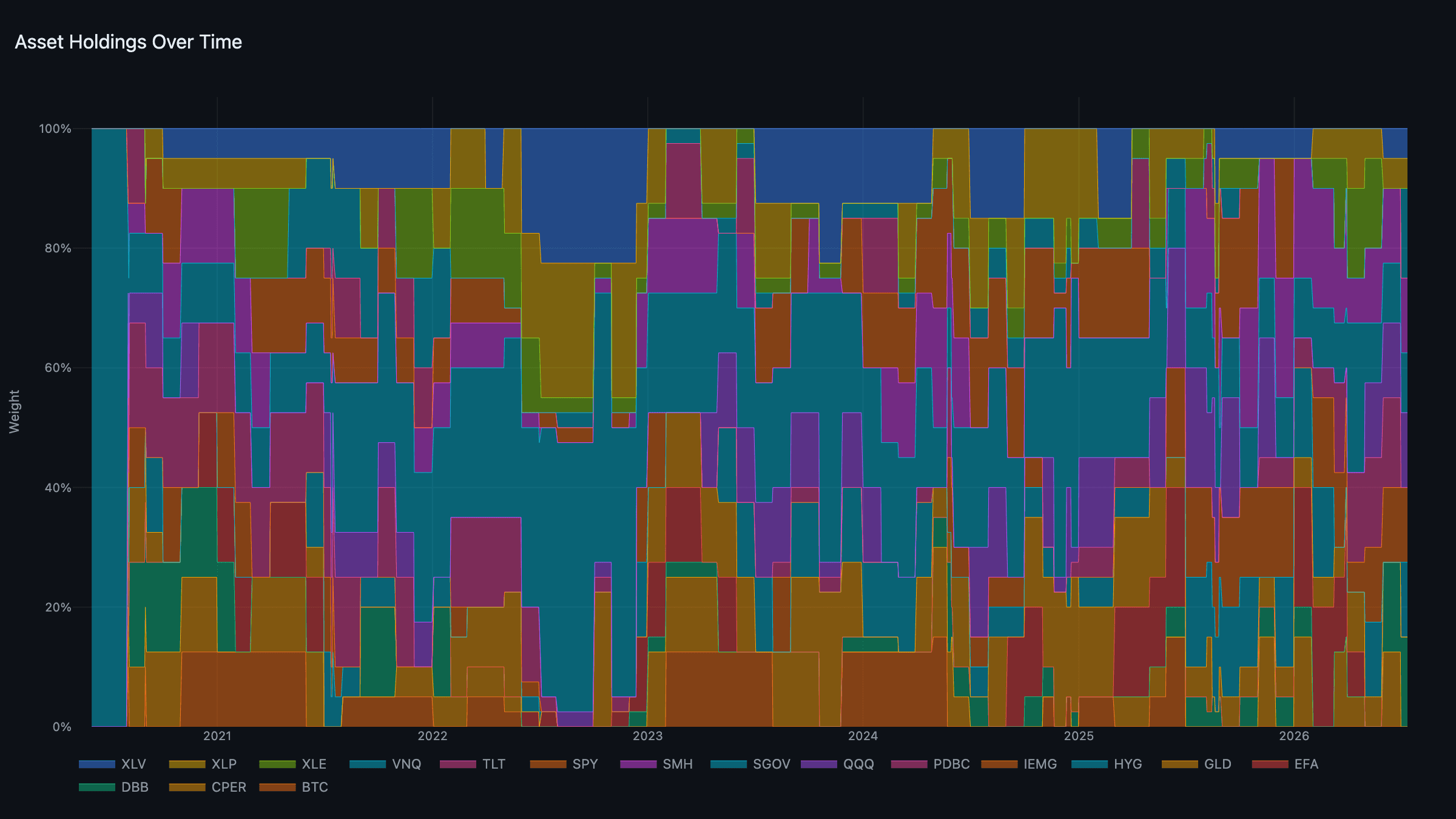

The Portfolio: QQQ Gets a New Neighbor

The book holds the rotation from the July 1st rebalance:

- Real assets: DBB + VNQ, 15% each.

- Growth: QQQ + SMH, 12.5% each.

- Liquidity: IEMG + HYG, 12.5% each.

- Defensive: XLV + XLP, 5% each.

- Cash: SGOV, 10%.

The notable development isn't a model rotation — it's an index one. Nasdaq confirmed SpaceX's addition to the Nasdaq-100, following its recent direct-listing restructuring, which puts it inside QQQ, one of the two names carrying the growth sleeve's full 12.5% weight. That's a mechanical shift in what the model actually holds, not a discretionary call: the sleeve tournament picked QQQ for its momentum characteristics, and the index committee just changed what QQQ is made of. Worth watching whether the addition's early volatility shows up in the sleeve's risk profile before the next rebalance.

News: A Polarizing Index Addition, and a Truce Collapses

Two stories dominated the week, and they're only connected by the calendar.

SpaceX's Nasdaq-100 inclusion reignited the market's most polarized personality debate. Elon Musk's companies have rarely traded on fundamentals alone, and this was no exception: the announcement drew both a wave of buying from investors who see SpaceX and the broader Musk ecosystem as an unmatched bet on the next decade of technology, and an equally loud backlash from a growing cohort that wants no exposure to Musk personally, citing his political entanglements and erratic public conduct. That backlash has a market expression now — a handful of "non-Elon" or Musk-exclusion ETFs, built to hold the S&P 500 or Nasdaq-100 minus every Musk-affiliated ticker, saw some of their largest inflows since launch this week. It's a small corner of the market in dollar terms, but a telling one: index inclusion used to be a purely mechanical event, and increasingly it's becoming a referendum on the man behind the ticker. For the framework, the practical point is narrower — QQQ's composition just changed, and that flows straight through to the growth sleeve's holdings whether or not you have a view on Musk himself.

Separately, and more consequentially for the macro picture, Iran formally broke off the peace framework it signed with the US barely weeks ago. What had been a slow-motion unraveling — a postponed Geneva session, flare-ups in Lebanon, a disputed Hormuz closure announcement — became explicit this week, with Tehran declaring the memorandum void and both sides resuming harder rhetoric. Brent, which had drifted back toward the low $80s on hopes the truce would hold, jumped sharply on the news and is now testing the highs last seen during the spring shock. The Strait of Hormuz is once again the binary risk: a genuine disruption there would flow directly into the pipeline-costs channel and could reverse months of inflation composite cooling in short order. Markets took the move seriously but not yet as a full risk-off signal — equities dipped intraday before recovering, consistent with a framework still reading the regime as Reflation, not stagflation.

Week Ahead

- Oil and Hormuz: The single most important variable for the inflation composite right now. A real disruption reverses the disinflation trend; a further cooling in rhetoric lets it continue.

- SpaceX / QQQ: Watching whether the addition's volatility shows up in the growth sleeve's risk metrics before the next scheduled rebalance.

- Growth's breadth: A +0.73 print is the strongest of the year — next week's data will show whether it's the start of a new leg higher or a single strong month.

All model scores are normalized to a [-1, +1] scale through our proprietary normalization methodology. Positive readings indicate above-trend expansion; negative readings indicate below-trend contraction. Data updated through July 10, 2026.

MacroScope models are systematic tools, not investment advice. Past performance does not guarantee future results.