MacroScope Weekly — July 5, 2026

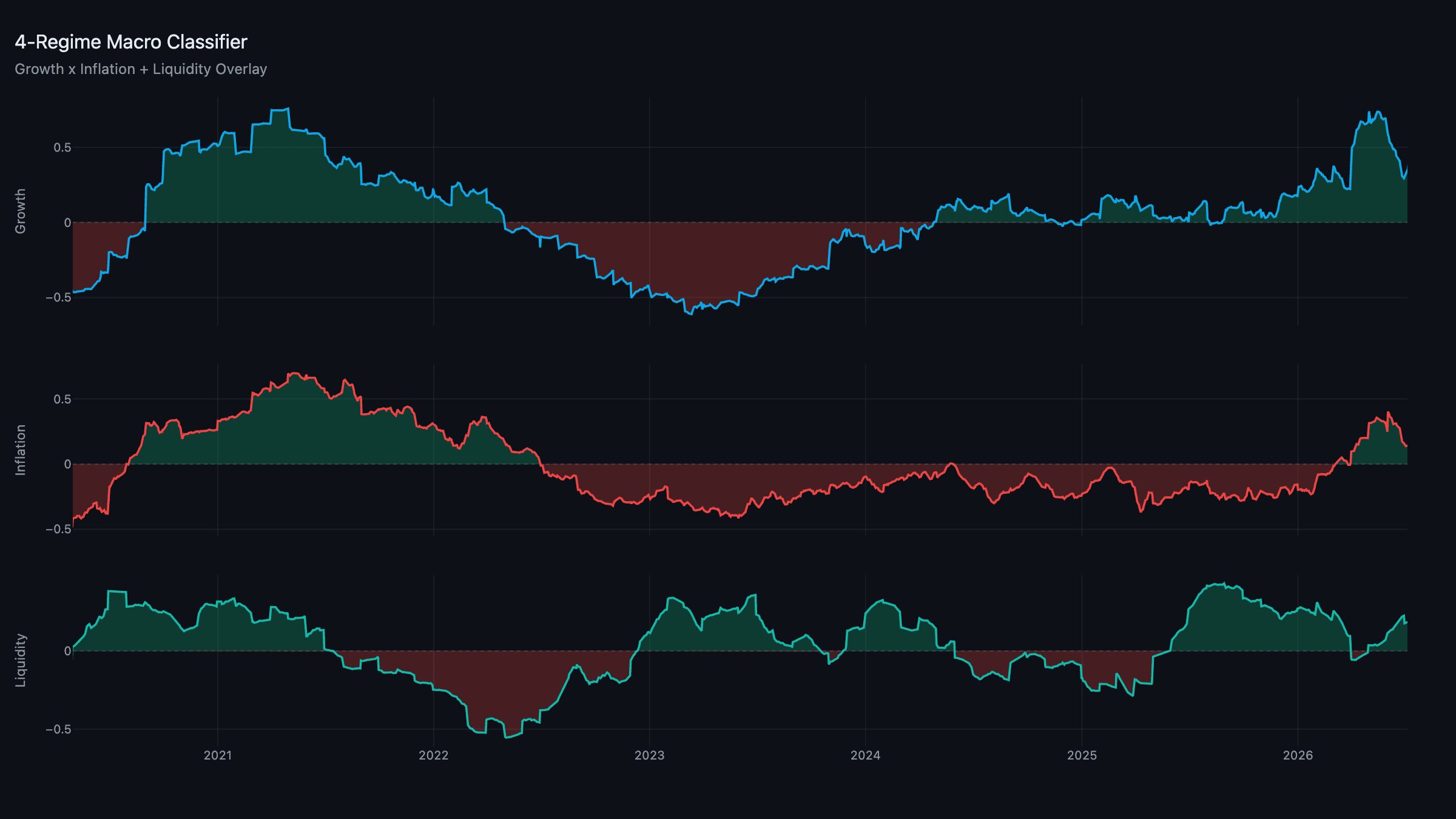

Current Regime: Reflation / Expanding Liquidity

TL;DR: Reflation / Expanding holds into the new month. Growth firmed to +0.34, inflation kept cooling to +0.14, and liquidity eased slightly to +0.18 but stayed on the Expanding side of the dead-band. The bigger story is under the hood: the July 1st sleeve rebalance rotated the book meaningfully toward growth and liquidity, and out of defensives and cash. It's the most aggressive posture the five-sleeve model has taken since it launched.

Composites: A Steady Reflation

Growth firmed modestly to +0.34, recovering from the pre-month-end pause, on continued strength in the AI/production cycle. Inflation extended its slide to +0.14 — the lowest print since the spring energy shock first broadened the composite — as the energy impulse keeps fading and services stay disinflationary. Liquidity eased slightly to +0.18 on a firmer dollar over the holiday week, but the pillar structure (repo, cross-border funding, collateral & funding) shows no stress; this reads as noise, not a turn.

The regime holds at Reflation / Expanding for a fourth straight week. With inflation now closer to zero than at any point since the shock began, the Goldilocks boundary is back in view — though the hysteresis band means it'll take a decisive move, not just a close call, to flip.

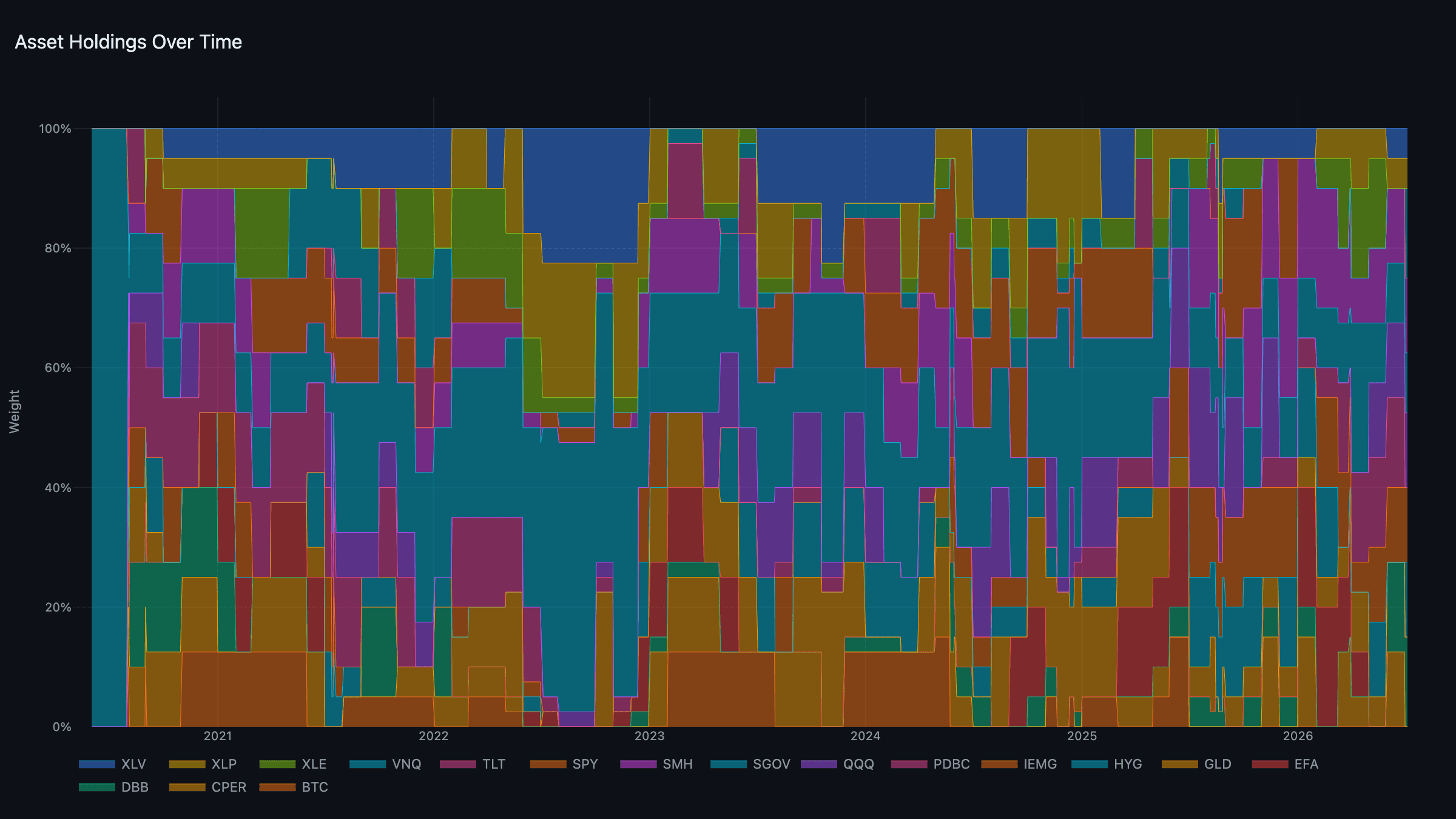

The Portfolio: The Book Turns Aggressive

The July 1st rebalance produced the sharpest rotation since the five-sleeve model launched:

- Real assets: DBB + VNQ, 15% each (PDBC rotates out, VNQ in — commodities give way to REITs).

- Growth: QQQ + SMH, 12.5% each, up from 7.5% — the tournament's strongest conviction call this cycle.

- Liquidity: IEMG + HYG, 12.5% each (CPER rotates out, HYG in — copper gives way to high-yield credit).

- Defensive: XLV + XLP, 5% each, down from 12.5%.

- Cash: SGOV, 10%, down from 20%.

Net effect: growth and liquidity sleeve weight roughly doubled to 25% each, while defensive and cash were cut by more than half combined. This is the tournament reading a market where growth is firming, inflation is fading, and liquidity is steady as a green light to lean in — a genuinely different signal than the defensive, cash-heavy June book. It's the clearest test yet of the new engine's willingness to move fast when the data lines up.

News: A Quiet Holiday Week, PCE Confirms the Cool-Down

Markets traded on light, holiday-shortened volume around the July 4th break. The one data point that mattered: the May PCE reading confirmed core inflation continuing to soften, with the Fed's preferred gauge easing toward the mid-2% range even as the headline number stayed elevated on the lagged energy pass-through. That's consistent with what the inflation composite has been signaling for weeks — this is a fading shock, not a new inflation regime — and it's a big part of why the sleeve tournament felt comfortable adding risk at the rebalance.

Geopolitically, the Iran truce held through the holiday week, though wire reports late Thursday flagged renewed friction over inspection terms — nothing that moved oil meaningfully, but a reminder that "fragile" is still the operative word. Fed officials were mostly quiet given the holiday calendar; the next real test of the hawkish June dot plot comes with the July FOMC meeting later this month.

Week Ahead

- June jobs report: The next read on whether the growth composite's strength is showing up in the labor data.

- Iran inspection talks: Thursday's friction is worth watching — a breakdown here is the fastest path back to an oil-driven inflation scare.

- The new book: With growth and liquidity sleeve weight near cycle highs, this is the least defensive the portfolio has been all year. Worth tracking whether conviction holds or fades over the next few weeks.

All model scores are normalized to a [-1, +1] scale through our proprietary normalization methodology. Positive readings indicate above-trend expansion; negative readings indicate below-trend contraction. Data updated through July 3, 2026.

MacroScope models are systematic tools, not investment advice. Past performance does not guarantee future results.