MacroScope Weekly — June 28, 2026

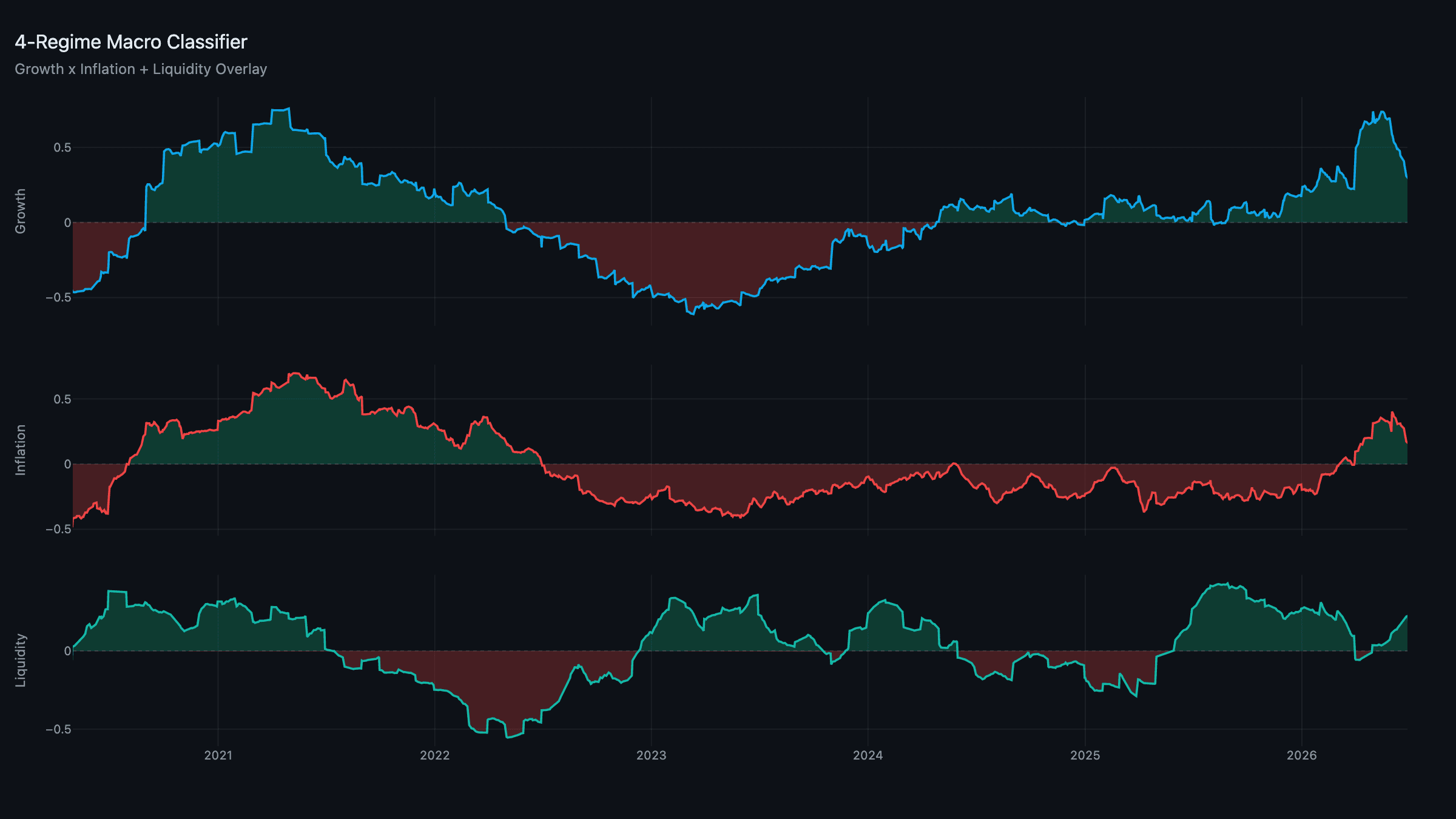

Current Regime: Reflation / Expanding Liquidity

TL;DR: Reflation / Expanding holds for a second week under the new hysteresis classifier. Growth eased to +0.31 as the post-FOMC data cools off, inflation kept fading to +0.17, and liquidity ticked up to +0.23 — still comfortably on the Expanding side of the line. It was a quiet week by this year's standards: no Fed meeting, no fresh Hormuz headlines, just a market digesting Warsh's hawkish dot plot and waiting on next week's PCE print. The book carries its June weights into the final week of the month.

Composites: A Cooling-Off Week

Growth eased to +0.31, down from +0.43 two weeks ago, as the production and distribution pillars gave back some of their post-FOMC strength — nothing alarming, just a normal pause after a strong run. Inflation kept drifting toward zero at +0.17, continuing the unwind of the spring energy impulse that's been the dominant inflation story all year. Liquidity firmed slightly to +0.23, helped by a steady dollar and no fresh funding stress in the collateral & funding pillar.

The regime stays Reflation / Expanding, and it's a boring week in the best sense: nothing moved enough to test the classifier's dead-band in either direction.

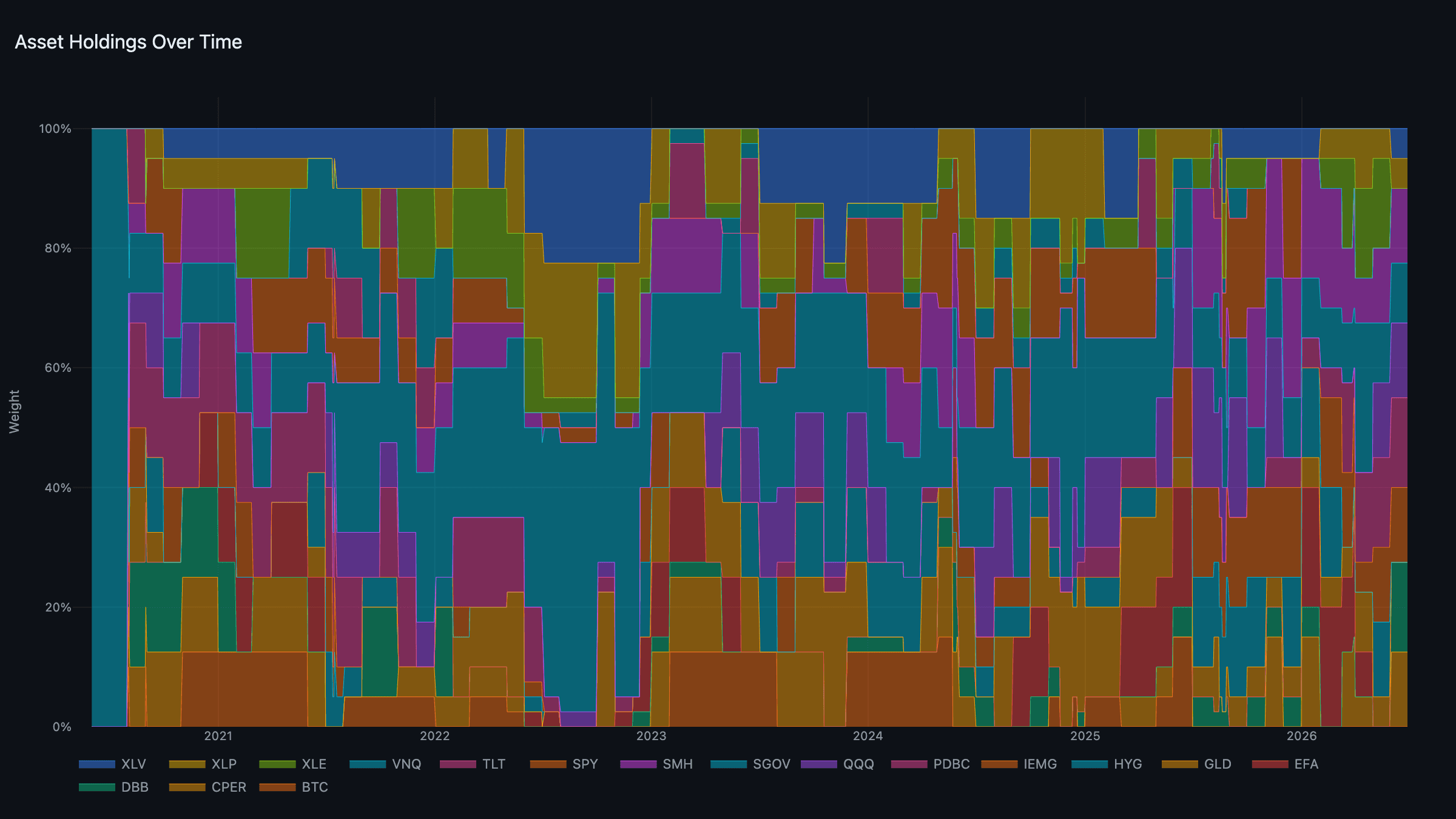

The Portfolio: Holding Into Month-End

No changes this week — the book runs out the last stretch of June unchanged:

- Real assets: DBB + PDBC, 15% each.

- Defensive: XLP + XLV, 12.5% each.

- Growth: QQQ + SMH, 7.5% each.

- Liquidity: IEMG + CPER, 5% each.

- Cash: SGOV, 20%.

With growth cooling and inflation still fading, the sleeve tournament has nothing decisive to act on before Tuesday's month-start rebalance. Worth watching: growth's pillars have been more volatile week-to-week under the new five-sleeve engine than under the old fixed basket, which is by design — the tournament is meant to rotate names as soon as momentum shifts, not wait for a scheduled rebalance.

News: A Rare Quiet Week

After a month dominated by the Warsh transition and the Iran conflict, this was the calmest news week since March. Fed officials mostly stuck to the script laid out in the June dot plot, with a couple of regional presidents reiterating that hikes remain "on the table, not the base case" — language markets read as somewhat less hawkish than the dots themselves implied. Equities drifted higher into month-end on light volume, typical of the week before a holiday-shortened session.

On the geopolitical front, the fragile Iran truce held for a second straight week without a fresh Hormuz scare, and Brent settled in the low $80s. That's a relief for the inflation composite, which has been leaning on exactly this kind of de-escalation to keep unwinding. The framework's read: quiet weeks like this one are when the underlying trend gets to reassert itself without a geopolitical shock distorting the signal.

Week Ahead

- May/June PCE: The Fed's preferred inflation gauge lands next week — the cleanest test yet of whether core pressure is genuinely rolling over.

- Month-start rebalance: The sleeve tournament gets its first scheduled look at July 1st data. With growth cooling and liquidity firming, don't be surprised if the growth and liquidity sleeves see a name change.

- Hormuz: Still the tail risk. A second calm week doesn't retire it, but it does earn the market's benefit of the doubt for now.

All model scores are normalized to a [-1, +1] scale through our proprietary normalization methodology. Positive readings indicate above-trend expansion; negative readings indicate below-trend contraction. Data updated through June 26, 2026.

MacroScope models are systematic tools, not investment advice. Past performance does not guarantee future results.