MacroScope Weekly — June 21, 2026

Current Regime: Reflation / Expanding Liquidity

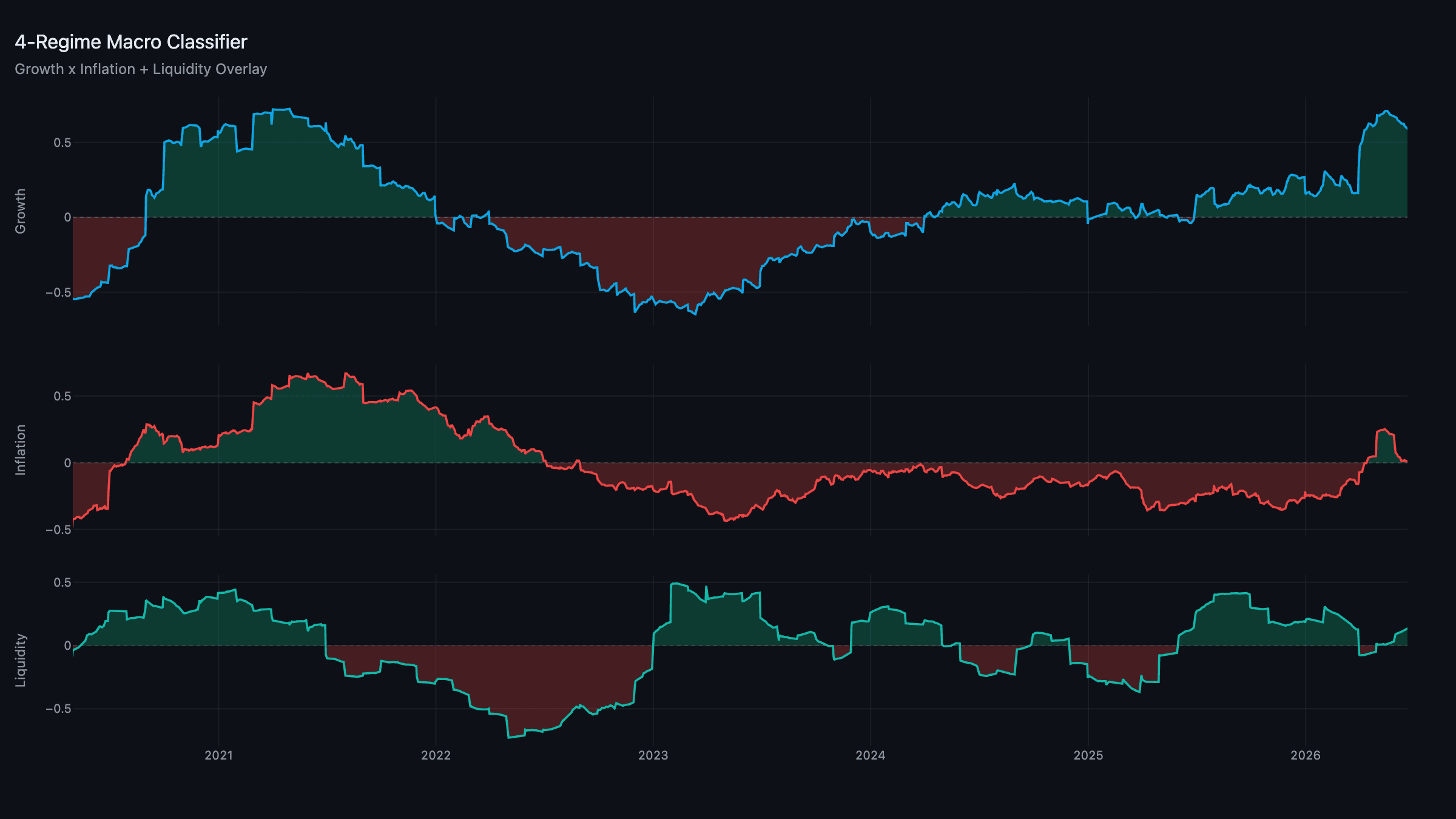

TL;DR: The regime holds at Reflation / Expanding — liquidity firmed to +0.13, growth eased to +0.60, inflation still flat at +0.01. Warsh's first FOMC delivered a unanimous hold wrapped in a distinctly hawkish dot plot: the median 2026 path now implies hikes, not cuts. Markets took it in stride because liquidity, by our read, is still expanding underneath the rhetoric. Geopolitics re-intruded late in the week — a peace MOU was signed, then Iran re-announced a Hormuz closure. And on the system side: this week we shipped the largest upgrade to the models since launch. Details below.

System Update: A Major Model Upgrade

Before the macro, the housekeeping — because it changes what you see on the dashboard. This week we rolled out a ground-up overhaul of the engine:

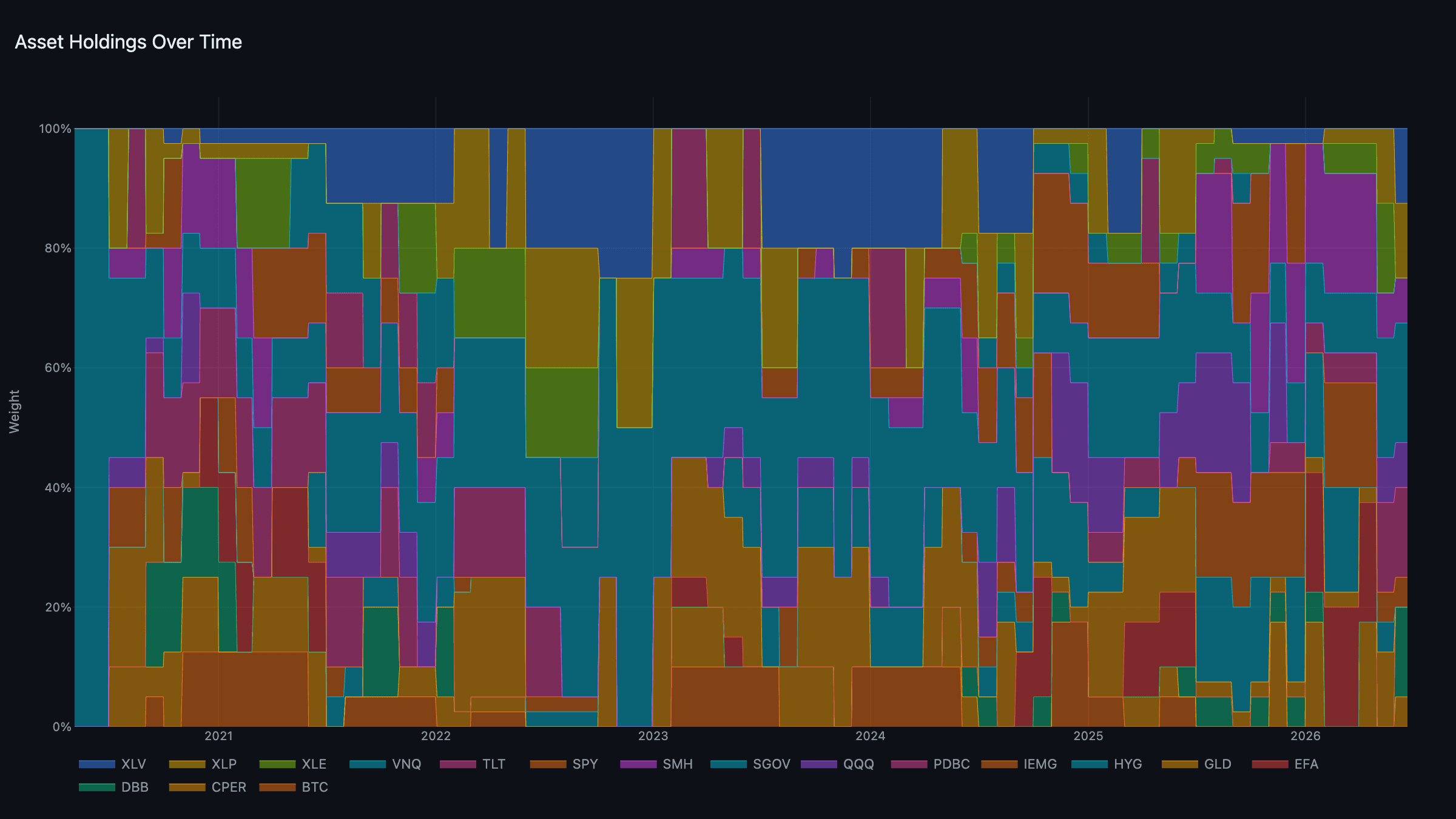

- The portfolio is now a five-sleeve tournament. Each regime sets weights across five purpose sleeves — growth, liquidity, real assets, defensive, and cash — and a vol-adjusted momentum tournament holds the two strongest names in each sleeve's pool. This replaces the old fixed-basket model and its on/off cash gate. Gold and bitcoin are no longer permanent anchors — gold competes in the defensive sleeve, bitcoin in the liquidity sleeve, held only when the cycle and momentum favour them. The tradable universe expanded from 7 names to 17.

- Liquidity is now five pillars, adding a Collateral & Funding pillar that reads stress in the repo, money-market, and volatility plumbing — the framework's new early-warning layer.

- Inflation is streamlined to five channels (the old import-prices channel was folded into pipeline costs), and the demand and services channels were rebuilt around faster, composition-adjusted data.

- The regime classifier now uses a hysteresis dead-band, so the regime only flips on a decisive move — no more whipsawing when a composite hovers around zero. You've seen this in action the last two weeks, with inflation sitting near the threshold without flipping the regime.

The methodology pages, model cards, and VAMS charts on the dashboard have all been updated to match. Backtested over 2020–present, the new model runs at roughly a 17% CAGR / 1.2 Sharpe / −13% max drawdown, comfortably ahead of buy-and-hold.

Composites: Liquidity Leads

Liquidity is now the strongest leg at +0.13 — the dollar's decline, improving cross-border funding, and a calm collateral & funding pillar are all pulling the same direction. Growth eased modestly to +0.60 but remains robustly positive on the AI/production cycle. Inflation is flat at +0.01, held on the Reflation side of the line by the new hysteresis band as the energy impulse continues to unwind.

The regime stays Reflation / Expanding. The honest nuance: with inflation hugging zero, this is one decisive move away from drifting back to Goldilocks — a better regime, not a worse one. The framework will let the data resolve it.

The Portfolio: Holding the Constructive Book

The June book is intact:

- Real assets: DBB + PDBC, 15% each.

- Defensive: XLP + XLV, 12.5% each.

- Growth: QQQ + SMH, 7.5% each.

- Liquidity: IEMG + CPER, 5% each.

- Cash: SGOV, 20%.

This is the new sleeve model's first full month live on the dashboard, and the book it's holding — cyclical real assets, quality defensives, measured growth, a copper-and-EM liquidity tilt, and a fifth in T-bills — is a clean expression of an expanding-liquidity, cresting-inflation regime.

News: A Hawkish Hold and a Fragile Peace

Kevin Warsh chaired his first FOMC on Wednesday. The Committee held at 3.50%–3.75% in a unanimous 12–0 vote — but the dot plot turned hawkish: the median 2026 path was raised to 3.8% (from 3.4% in March), nine of eighteen participants now pencil in hikes by year-end, and seventeen of eighteen see inflation risks tilted to the upside. Notably, the new chair declined to place his own dot. A Fed openly debating hikes into an energy shock is the debt-refinancing trap in plain view — tightening is exactly what the fiscal arithmetic can least afford.

Markets shrugged, and the framework explains why: the price of money rhetoric is hawkish, but the quantity of liquidity — what the composite actually measures — is still expanding. On geopolitics, a memorandum to end the Iran conflict was signed midweek, then promptly undercut: US–Iran talks in Geneva were abruptly postponed, fighting flared in Lebanon, and Iran re-announced a Strait of Hormuz closure (which the US disputed). Brent, which had fallen toward $80 on easing supply fears, is the live wire — a genuine re-closure would re-light the inflation impulse the composite just watched fade.

Week Ahead

- PCE (late June): The Fed's preferred gauge — confirmation of whether core pressure is genuinely cooling beneath the energy-driven headline.

- Hormuz / oil: The binary risk. A real re-closure flips inflation back up and could pull the regime; a de-escalation cements the Goldilocks drift.

- The overlay: Watch whether Expanding liquidity survives a hawkish new chair. It's the linchpin of the constructive posture — and now you can watch the new Collateral & Funding pillar for the first sign of any stress.

All model scores are normalized to a [-1, +1] scale through our proprietary normalization methodology. Positive readings indicate above-trend expansion; negative readings indicate below-trend contraction. Data updated through June 19, 2026.

MacroScope models are systematic tools, not investment advice. Past performance does not guarantee future results.