MacroScope Weekly — June 7, 2026

Current Regime: Reflation / Expanding Liquidity

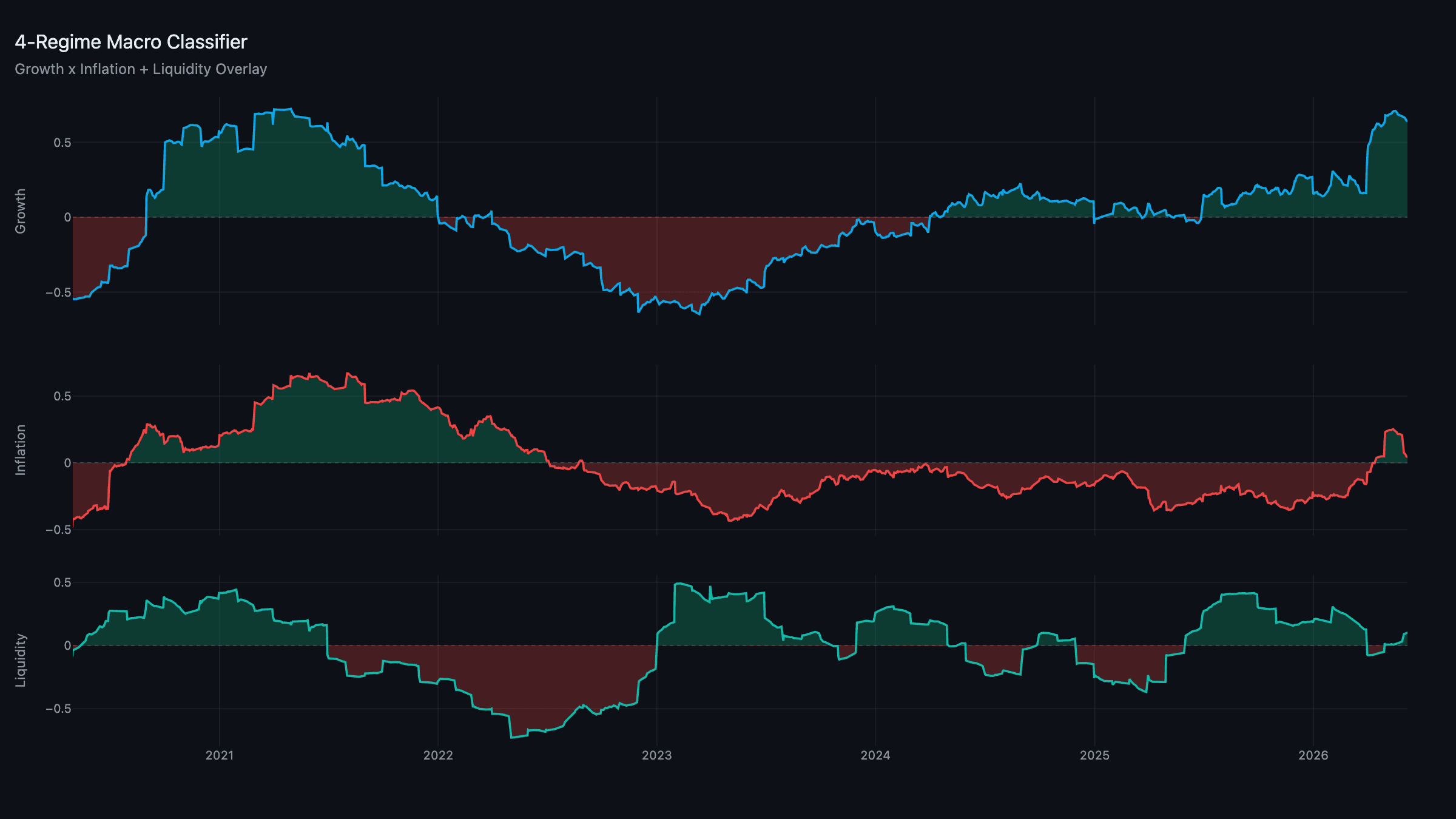

TL;DR: The upgrade landed. Liquidity confirmed its flip to positive at the month-start rebalance — the composite is now +0.10 — and the overlay turned Expanding for the first time since the energy shock began. With growth still strong (+0.65) and inflation fading back toward zero (+0.05), the regime is now Reflation / Expanding: the most constructive backdrop the framework has read all year. The book rotated accordingly. The S&P printed a fresh record above 7,600 on Tuesday before a sharp tech-led pullback Friday on rising rate-hike odds.

Composites: Liquidity Turns the Corner

Two big moves. Liquidity flipped to +0.10, decisively clearing the dead-band — the dollar has rolled over, cross-border dollar funding is improving, and the collateral & funding pillar has calmed as the conflict's acute phase eases. And inflation faded to +0.05: oil is off its highs, and while the year-over-year energy comparison is still ugly, the rate of change the composite measures has rolled over. Growth is unchanged at a robust +0.65.

Reflation with Expanding liquidity is the quadrant the debt-refinancing thesis points to as the sweet spot — growth intact, the inflation impulse cresting, and liquidity actively supportive. It's the green light the risk side of the book has been waiting two months for.

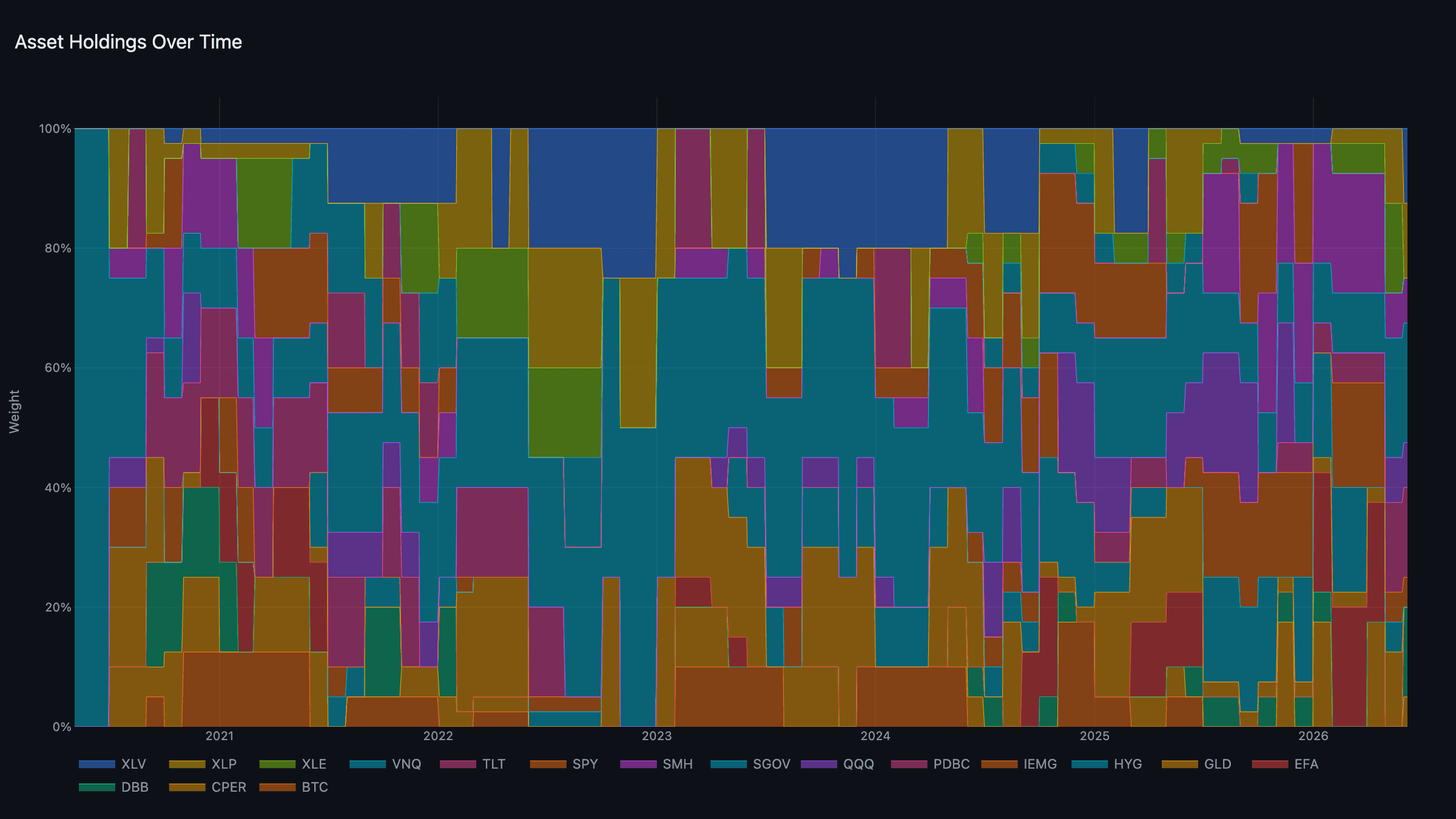

The Portfolio: The Rotation Fires

The regime change rewired the book at the rebalance:

- Real assets: DBB + PDBC — base metals join broad commodities as energy's relative leadership fades; XLE drops out of the sleeve.

- Defensive: XLP + XLV — staples and healthcare; gold no longer wins the defensive sleeve, a direct consequence of the inflation impulse cresting and liquidity turning supportive.

- Growth: QQQ + SMH — US large-cap tech reclaims a spot alongside semis as the AI rally broadens.

- Liquidity: IEMG + CPER — emerging markets and copper on the weaker dollar.

- Cash: SGOV, 20%.

The gold-out, base-metals-and-healthcare-in shift is the system reading a regime where you no longer need the maximum inflation hedge — you want cyclical and quality exposure into an expanding-liquidity tape.

News: A Record, Then a Reckoning

The S&P closed at a record 7,609 on Tuesday — its first-ever close above 7,600 and the cap to a nine-session win streak, the longest in over a year. Leadership was exactly what you'd expect: Nvidia jumped on a new PC-class chip launch, the cloud-computing complex surged, and the AI-infrastructure trade broadened beyond the usual handful of names.

Then Friday bit back — the worst session of the year, with AI stocks tumbling as rate-hike odds climbed into next week's CPI and the Warsh Fed's first meeting. That's a healthy reminder that a record built on a concentrated leadership group reprices fast when the rate narrative shifts. The framework's response is unchanged: hold the strongest names across five sleeves and let the regime, not the daily tape, set the posture.

Week Ahead

- May CPI (Jun 10): The pivotal print. The composite says the inflation impulse is cresting; CPI will confirm or deny it. A hot energy-driven headline with cool core would validate the framework's read.

- FOMC (Jun 16–17): Warsh's first meeting as chair, with a fresh dot plot. The single biggest event for the liquidity composite.

- Hold of the upgrade: Watch whether Expanding liquidity sticks — the whole bullish case rests on it.

All model scores are normalized to a [-1, +1] scale through our proprietary normalization methodology. Positive readings indicate above-trend expansion; negative readings indicate below-trend contraction. Data updated through June 5, 2026.

MacroScope models are systematic tools, not investment advice. Past performance does not guarantee future results.