MacroScope Weekly — May 31, 2026

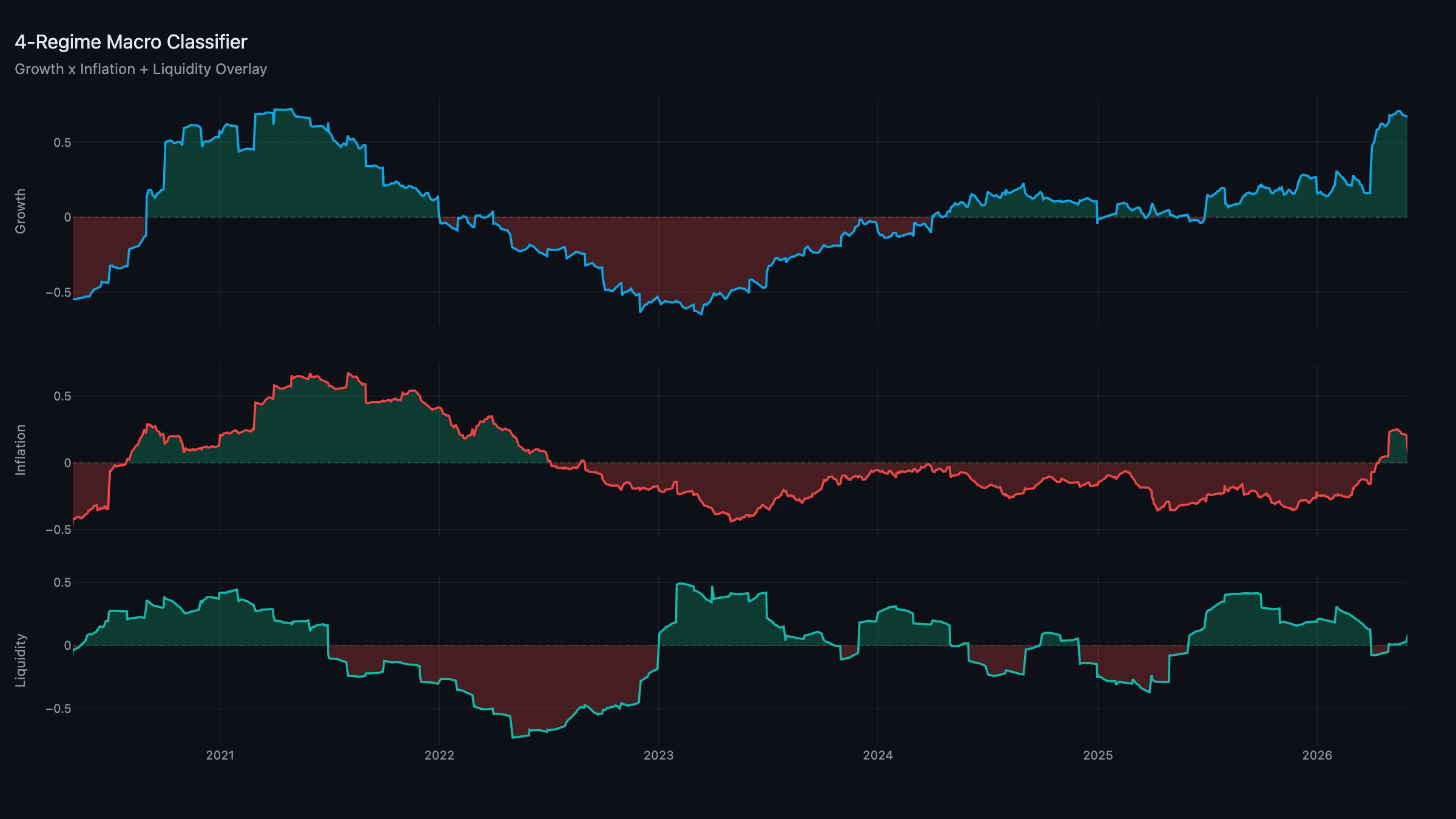

Current Regime: Reflation / Contracting Liquidity

TL;DR: Last week of Reflation / Contracting — but only just. Growth holds at +0.67, inflation at +0.21, and liquidity firmed again to +0.03, still a hair inside the dead-band. The composite is on the cusp of flipping the overlay to Expanding, and the month-start rebalance will catch it if it does. Equities are pressing toward record highs as tech leadership reasserts, even with oil still elevated. This is the calm before a likely regime upgrade.

Composites: One Notch From Expanding

Growth and inflation are steady — +0.67 and +0.21 — keeping the quadrant firmly Reflation. The action is in liquidity, which has now strung together a few positive readings and sits at +0.03. It's still inside the ±0.05 hysteresis band, so the overlay reads Contracting for one more week, but the trajectory is unambiguous: central-bank balance sheets are stabilising, the dollar continues to ease, and funding stress has drained as the conflict's acute phase passes.

The framework is built to be patient here. The dead-band means liquidity has to earn the flip — but it's close, and a confirmed move to Expanding would mark the first genuine risk-on green light since the energy shock began.

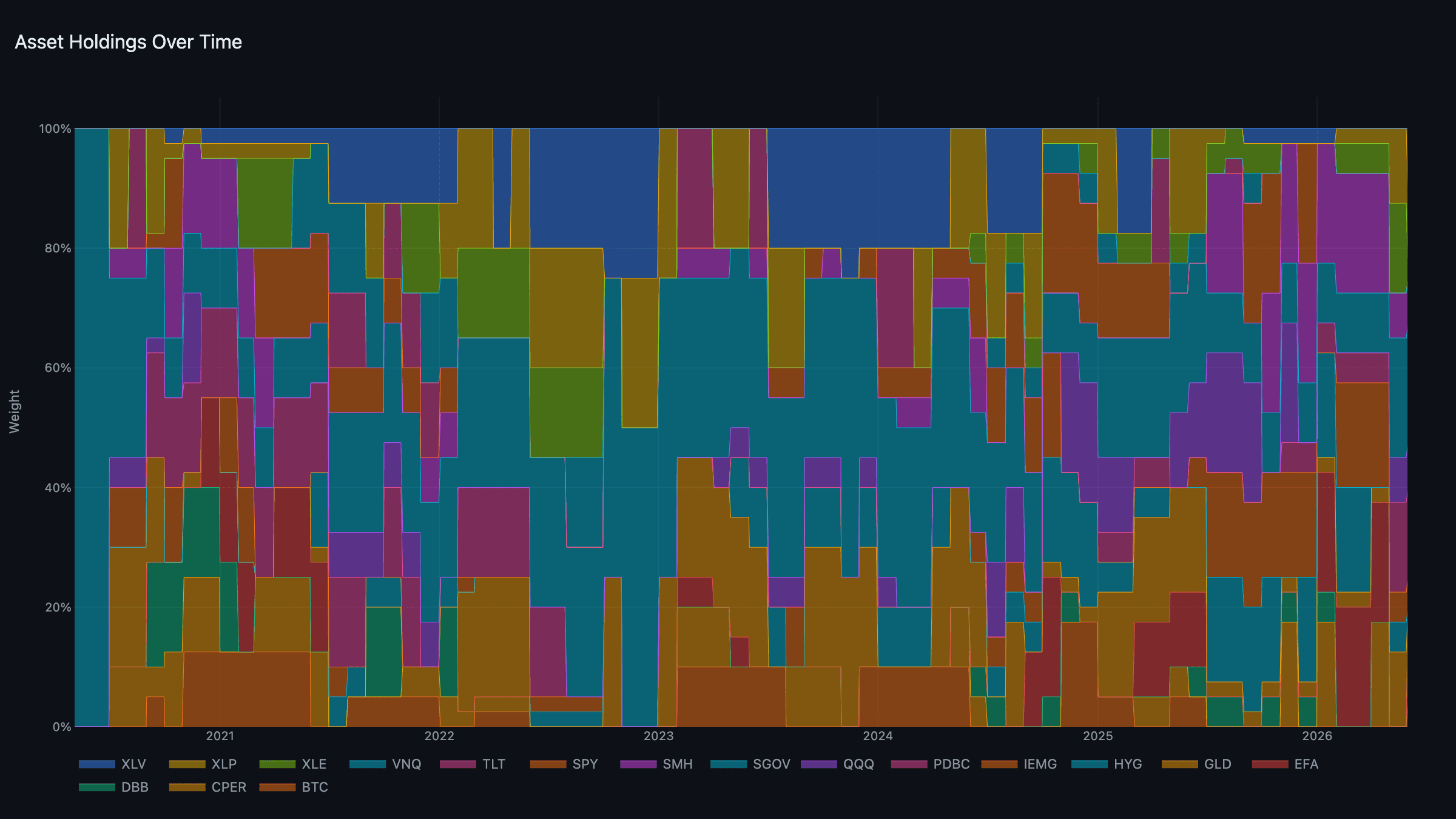

The Portfolio: On the Cusp of Rotation

The book is unchanged for one final week — PDBC + XLE, GLD + XLP, SGOV 20%, SMH + QQQ, IEMG + HYG — but it's poised to move. If liquidity confirms Expanding at the month-start rebalance, the regime shifts to Reflation/Expanding and the sleeve weights tilt back toward growth and liquidity, with the defensive sleeve lightening and gold's outsized role stepping down.

This is the cleanest illustration of why the system rebalances monthly rather than reacting day to day: it lets a borderline signal resolve, then acts decisively once, rather than flickering in and out on noise around the zero line.

News: Records in Sight

Despite triple-digit-adjacent oil and a four-month inflation scare, US equities are pressing toward all-time highs into month-end. The driver is familiar: semiconductors and the broader AI-infrastructure complex, with the cloud and chip names leading breadth higher. The market is making a clear statement — it views the energy shock as a tax on the consumer, not a threat to the earnings engine of the megacap tech and AI build-out.

That's a coherent read with the framework's growth composite at +0.67. The risk is concentration: a rally carried by a handful of leaders is more fragile than a broad one. The model's answer is the tournament — it holds the strongest names but spreads across five sleeves, so it participates without betting the book on any single trade.

Week Ahead

- Month-start rebalance: The key event. A confirmed liquidity flip to Expanding triggers a rotation toward risk.

- May jobs report: A read on whether the labor market is still absorbing the energy shock without cracking.

- Records and oil: Watch whether equities can print new highs while oil stays bid — and whether any fresh Hormuz headline interrupts the grind.

All model scores are normalized to a [-1, +1] scale through our proprietary normalization methodology. Positive readings indicate above-trend expansion; negative readings indicate below-trend contraction. Data updated through May 29, 2026.

MacroScope models are systematic tools, not investment advice. Past performance does not guarantee future results.