MacroScope Weekly — May 24, 2026

Current Regime: Reflation / Contracting Liquidity

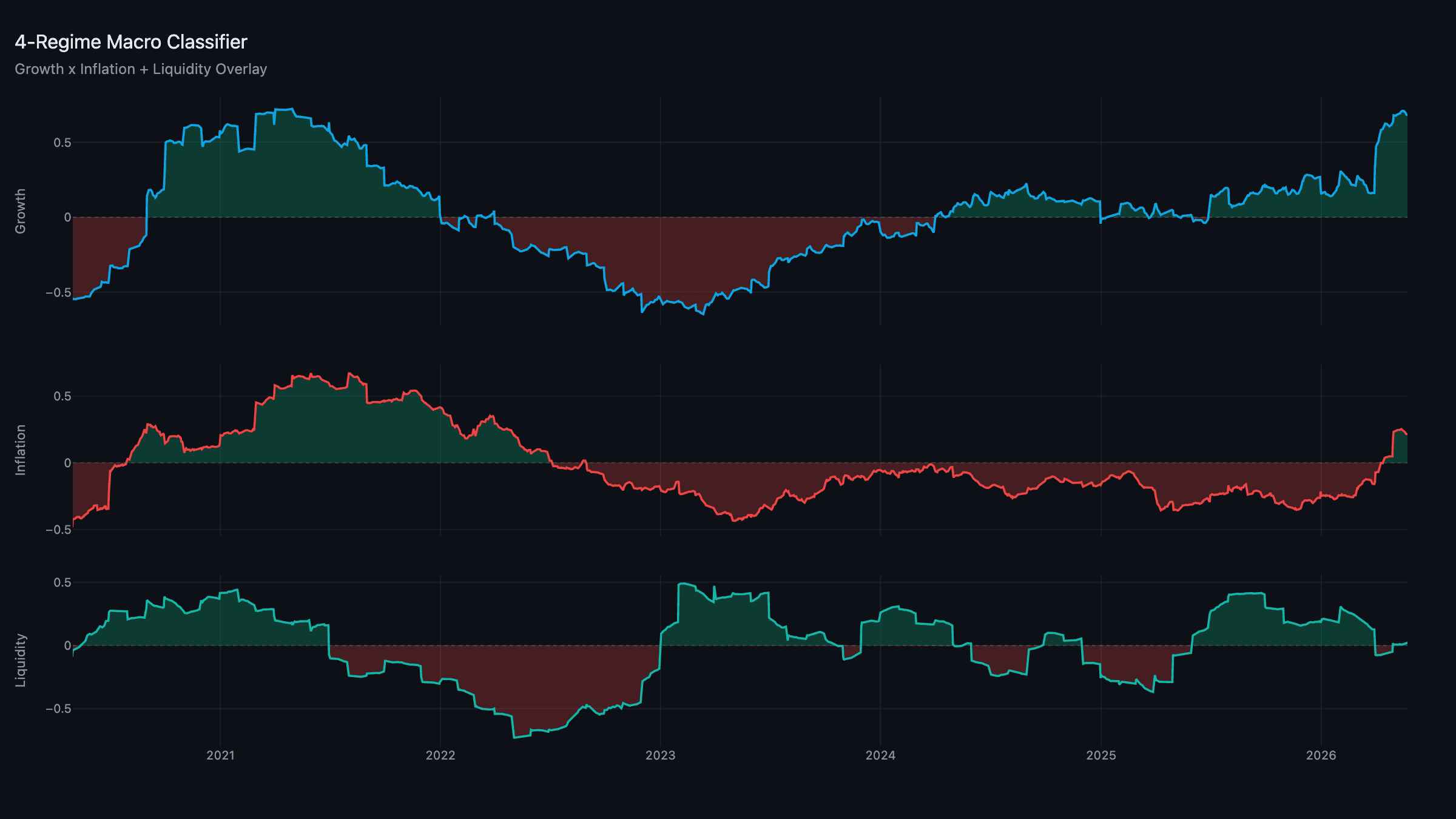

TL;DR: Reflation / Contracting holds into a fourth week. Growth eased a touch to +0.69 and inflation to +0.21 — both still firmly in Reflation territory — while liquidity crept up to +0.02, just barely positive but still inside the dead-band, so the overlay stays Contracting for now. Kevin Warsh was sworn in as Fed chair this week. The book is unchanged, and the most interesting tell in the framework is that liquidity is quietly trying to turn.

Composites: Liquidity Stirs

The headline numbers barely moved — growth +0.69, inflation +0.21 — but the liquidity composite is doing something worth flagging. It ticked up to +0.02, its first positive print in weeks. That's still inside the ±0.05 hysteresis band, so the regime classifier hasn't flipped the overlay — it requires a more decisive move before it changes state, which is the whole point of the dead-band: to avoid whipsawing on noise around zero.

But the direction matters. Cross-border dollar liquidity is improving as the greenback softens off its highs, and the funding-stress pillar has calmed as rate volatility eases from the conflict's peak. If this holds, the overlay flips to Expanding — and that's the upgrade the risk side of the book is waiting on.

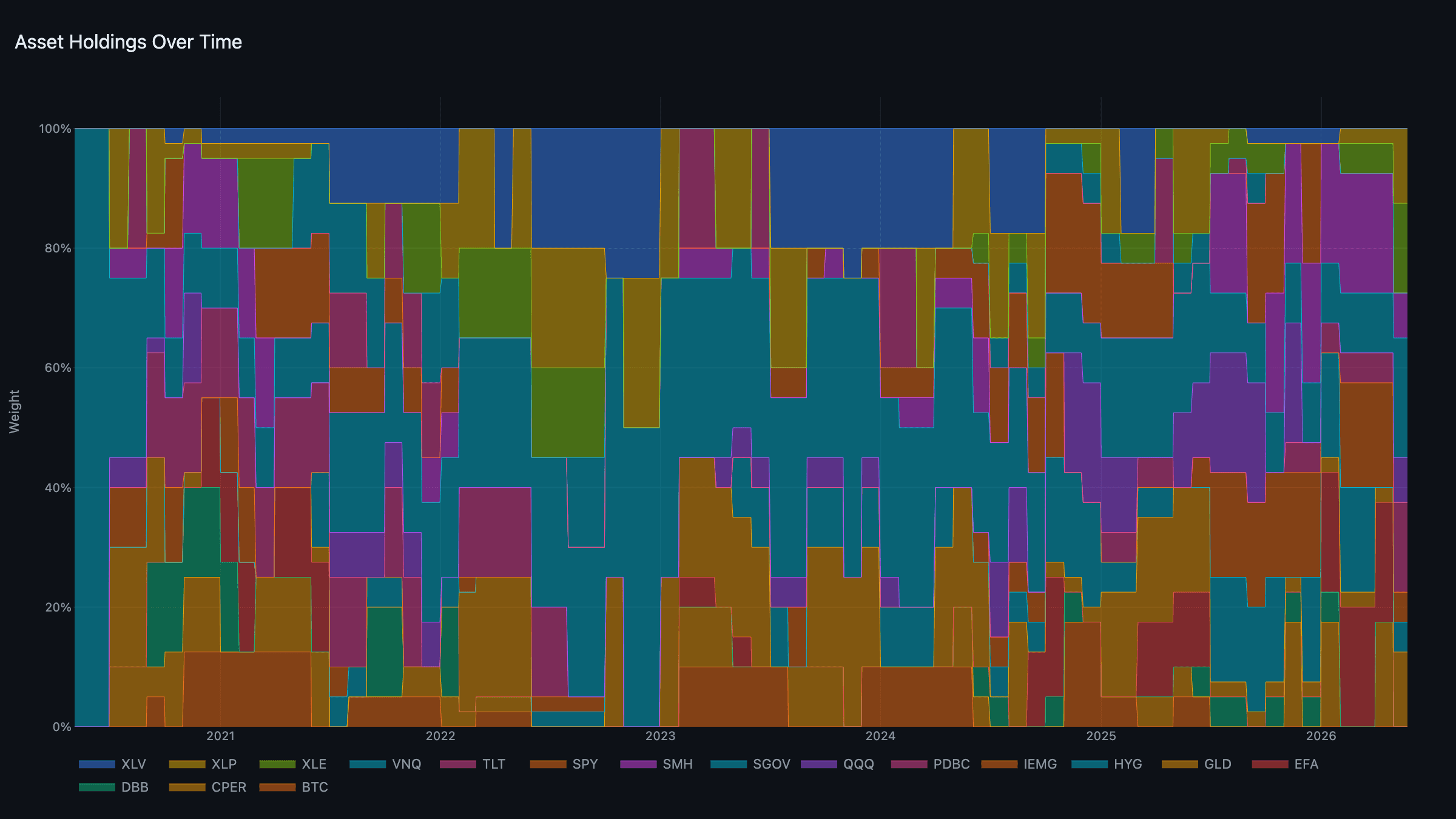

The Portfolio: Holding the Line

No regime change means no rotation. The book remains:

- Real assets: PDBC + XLE, 15% each.

- Defensive: GLD + XLP, 12.5% each.

- Cash: SGOV, 20%.

- Growth / Liquidity: SMH + QQQ, IEMG + HYG.

Gold has been the quiet workhorse of this regime — it's the asset that does well in both the inflation scare and the liquidity-uncertainty axis, which is why it keeps winning the defensive sleeve. If liquidity flips Expanding next month, expect the sleeve weights to shift back toward growth and liquidity and gold's role to step down.

News: The Warsh Era Begins

Kevin Warsh was sworn in as the 17th chair of the Federal Reserve this week, completing the handover from Jerome Powell. His first FOMC meeting as chair is just under a month away.

Markets have so far given him the benefit of the doubt — equities are firm, the dollar is easing, and the front end is stable. The open question is whether a chair with hawkish instincts validates the market's hope for eventual easing or leans into the inflation fight that the energy shock has handed him. The framework doesn't have to guess: the liquidity composite will tell us which way the plumbing is actually moving, regardless of the rhetoric. Right now it's inching toward easier — we'll see if that survives contact with a new chair.

Week Ahead

- Month-end rebalance: The model rebalances at the start of next month. If the liquidity overlay confirms its flip to Expanding, expect a meaningful rotation in the book.

- PCE / inflation data: The Fed's preferred gauge will either confirm or complicate the CPI-driven inflation picture.

- Oil: Holding in the low-$90s. A break in either direction reshapes the inflation composite into June.

All model scores are normalized to a [-1, +1] scale through our proprietary normalization methodology. Positive readings indicate above-trend expansion; negative readings indicate below-trend contraction. Data updated through May 22, 2026.

MacroScope models are systematic tools, not investment advice. Past performance does not guarantee future results.