MacroScope Weekly — May 10, 2026

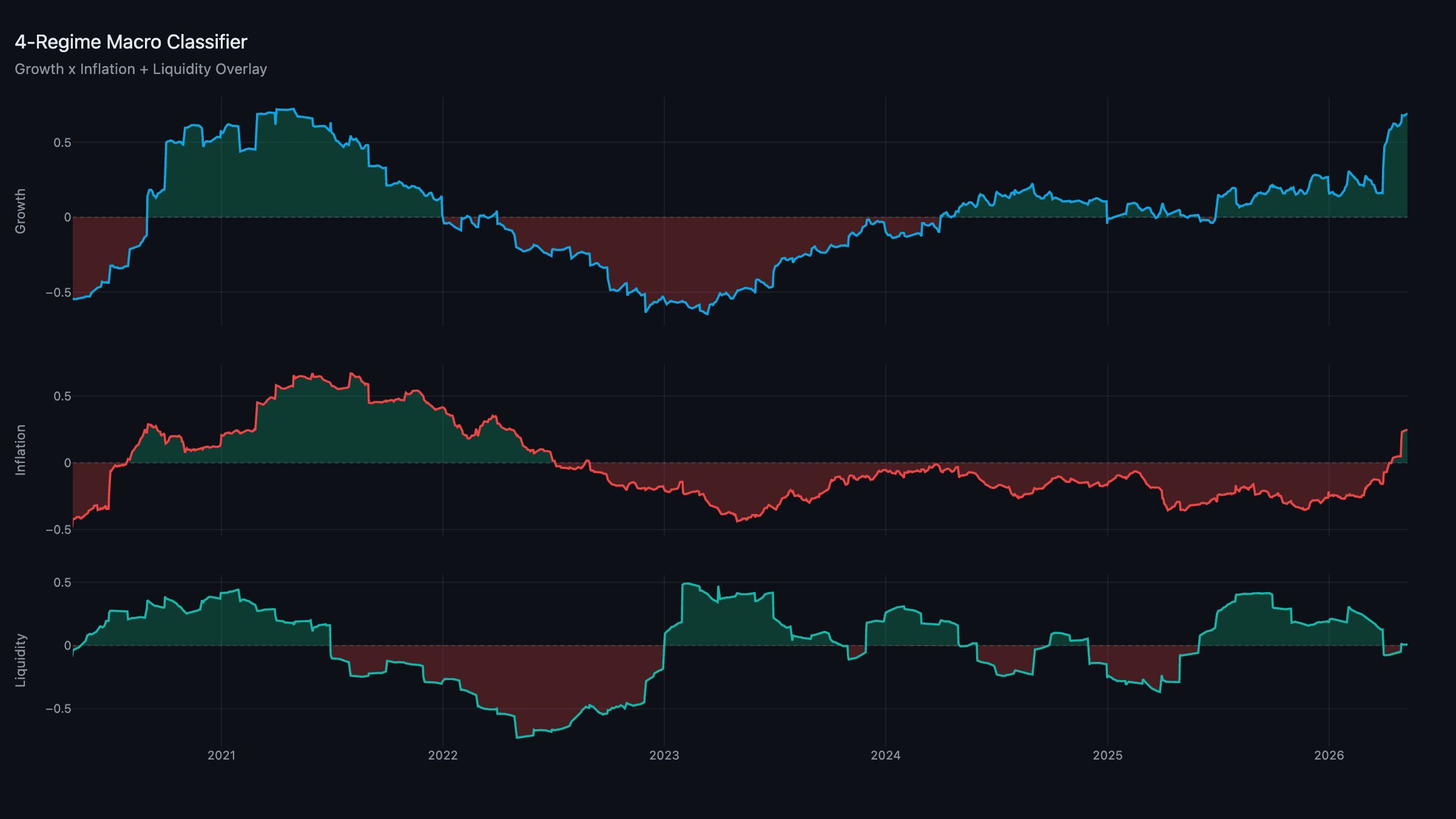

Current Regime: Reflation / Contracting Liquidity

TL;DR: No regime change — Reflation / Contracting holds for a second week, and if anything it firmed up: inflation ticked to +0.25 while growth stayed pinned near +0.68. The book is unchanged, anchored in real assets, gold, and a fat cash sleeve. The macro week was quiet on policy but loud on price: oil held in the low-$90s (WTI), and the market's attention has shifted to next week's Warsh confirmation vote and the April CPI print.

Composites: Reflation Entrenches

The story is consistency. Inflation is now firmly positive and still rising at the margin — the pipeline-costs channel keeps absorbing the energy shock, and the supply-chain pressure reading hasn't eased while Hormuz traffic stays depressed. Growth is unmoved near +0.68: the AI/semis capex cycle and resilient production are doing the heavy lifting, and there's no crack in the activity data yet.

Liquidity is the only thing keeping this from being an outright risk-on regime. The composite is hovering just below zero — central banks are frozen by the inflation scare and the dollar is firm — so the overlay stays Contracting. Two weeks in, Reflation looks entrenched rather than transitional.

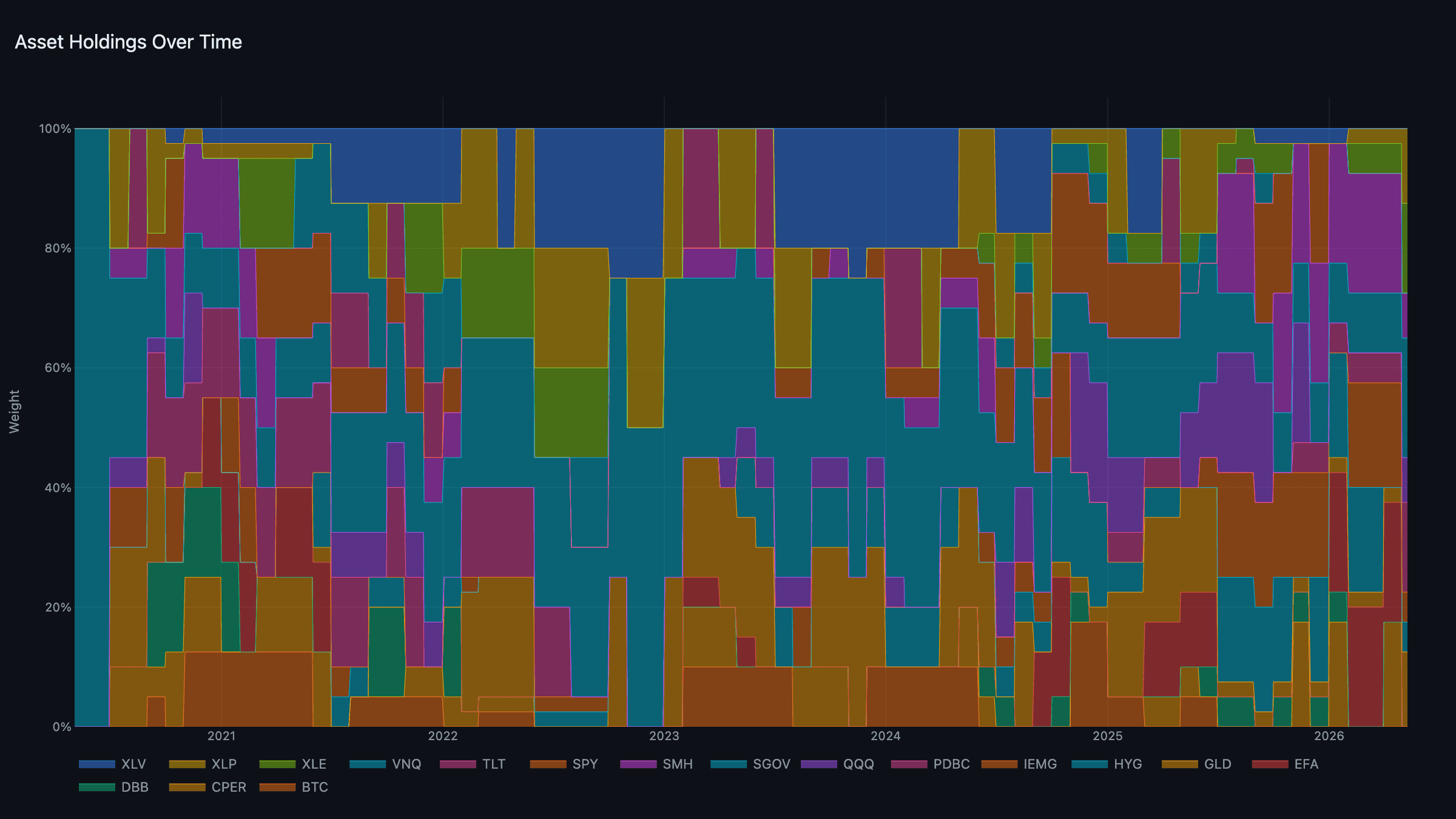

The Portfolio: Steady Hands

With the regime stable, the tournament held its book — no turnover, which is exactly what you want in a confirmed regime:

- Real assets: PDBC + XLE at 15% each — still the heaviest sleeve.

- Defensive: GLD + XLP at 12.5% each — gold continuing to earn its keep as the inflation hedge.

- Cash: SGOV at 20%.

- Growth / Liquidity: SMH + QQQ and IEMG + HYG filling out the rest at reduced weight.

The discipline point: in a Contracting-liquidity regime the model deliberately keeps a fifth of the book in T-bills earning the front-end yield. That's not timidity — it's the regime's prescription, and it's what lets the risk sleeves run without over-committing.

News: Quiet Policy, Loud Prices

A lighter week for scheduled events let the energy story breathe. Oil consolidated in the low-$90s WTI as Hormuz traffic stayed throttled but no fresh escalation hit the tape. Equities were choppy but resilient — the index is grinding, not breaking, and breadth has quietly improved as the energy and industrial names that the framework favours take leadership from the mega-cap complex.

Underneath, the inflation data is the thing to watch. With headline CPI already running near 4% and energy still climbing year-over-year, the April print due next week could be the one that forces the rate-hike conversation into the open.

Week Ahead

- Warsh confirmation vote (expected ~May 13): The full Senate is expected to vote on Kevin Warsh's nomination. A confirmation closes the succession question and sets up the handover from Powell, whose term expires mid-month.

- April CPI: The key print. A hot number cements Reflation and pulls hike odds forward; a cooler one would be the first hint the energy pass-through is peaking.

- Oil: Unchanged as the master variable — the inflation composite lives and dies on the Hormuz headlines.

All model scores are normalized to a [-1, +1] scale through our proprietary normalization methodology. Positive readings indicate above-trend expansion; negative readings indicate below-trend contraction. Data updated through May 8, 2026.

MacroScope models are systematic tools, not investment advice. Past performance does not guarantee future results.