MacroScope Weekly — May 3, 2026

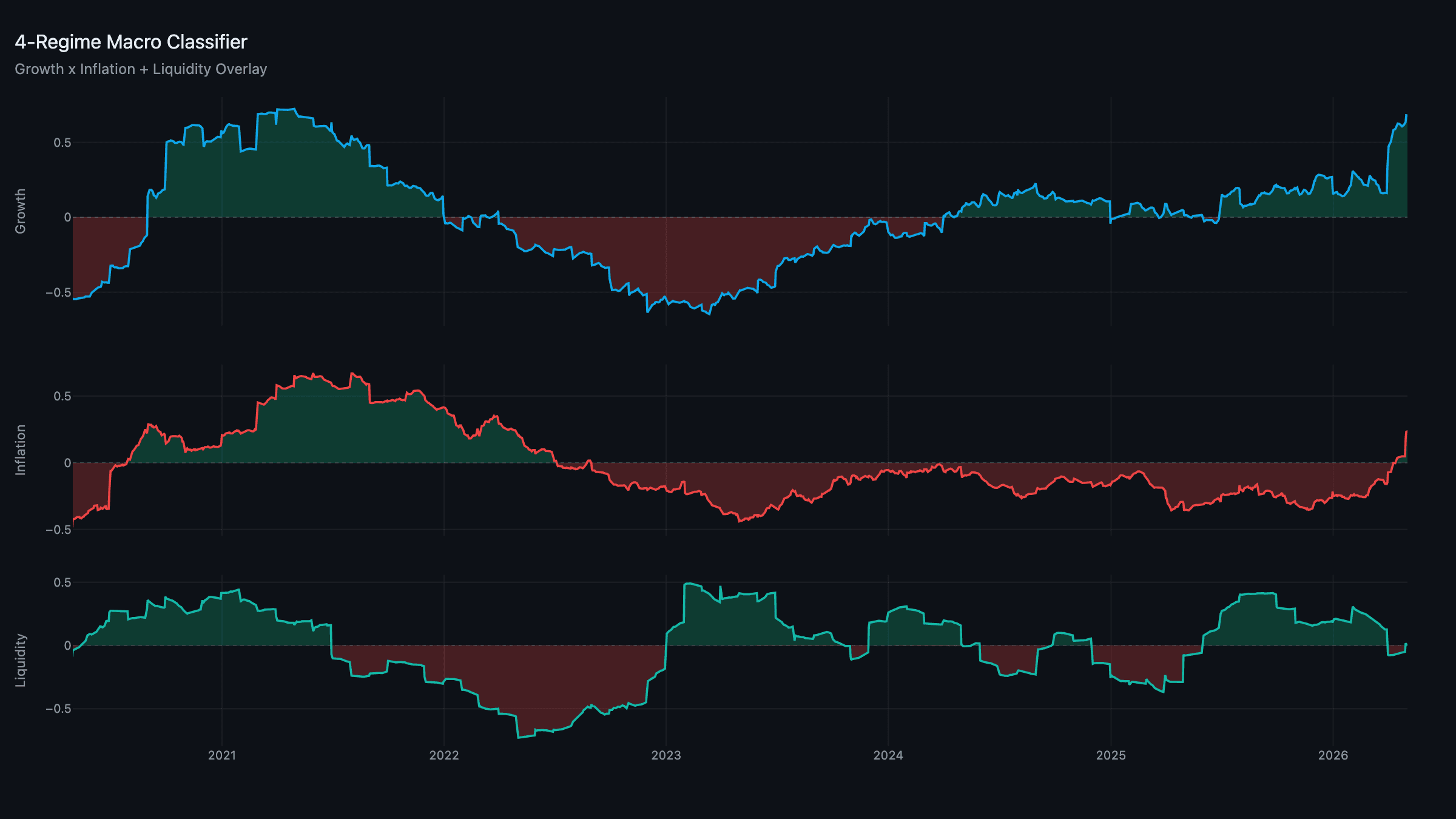

Current Regime: Reflation / Contracting Liquidity

TL;DR: The regime flipped. The energy shock has finally broadened through the inflation composite — it jumped from roughly flat to +0.23 as the Hormuz premium feeds pipeline costs — and with growth still strong, that moves us out of Goldilocks and into Reflation. Liquidity is still soft, so the overlay stays Contracting. The Fed held rates Wednesday in a remarkably fractured 8–4 vote, the most dissents since 1992. The portfolio has rotated hard toward real assets and cash.

Composites: Inflation Joins the Party

For two months the framework called this Goldilocks — strong growth, contained inflation. That ended this week. The inflation composite cleared the dead-band decisively, driven by the pipeline-costs channel: triple-digit oil, firm industrial metals, and a supply-chain pressure reading that won't normalise while the Strait of Hormuz is throttled. Growth is still humming near +0.68, so the growth-plus-rising-inflation quadrant is Reflation.

Liquidity remains marginally negative — central banks aren't easing into an inflation scare, and the dollar is firm — so the overlay holds at Contracting. Reflation with tightening liquidity is the classic "good growth, bad price stability" regime: you want hard assets, you want pricing power, and you want a real cash buffer.

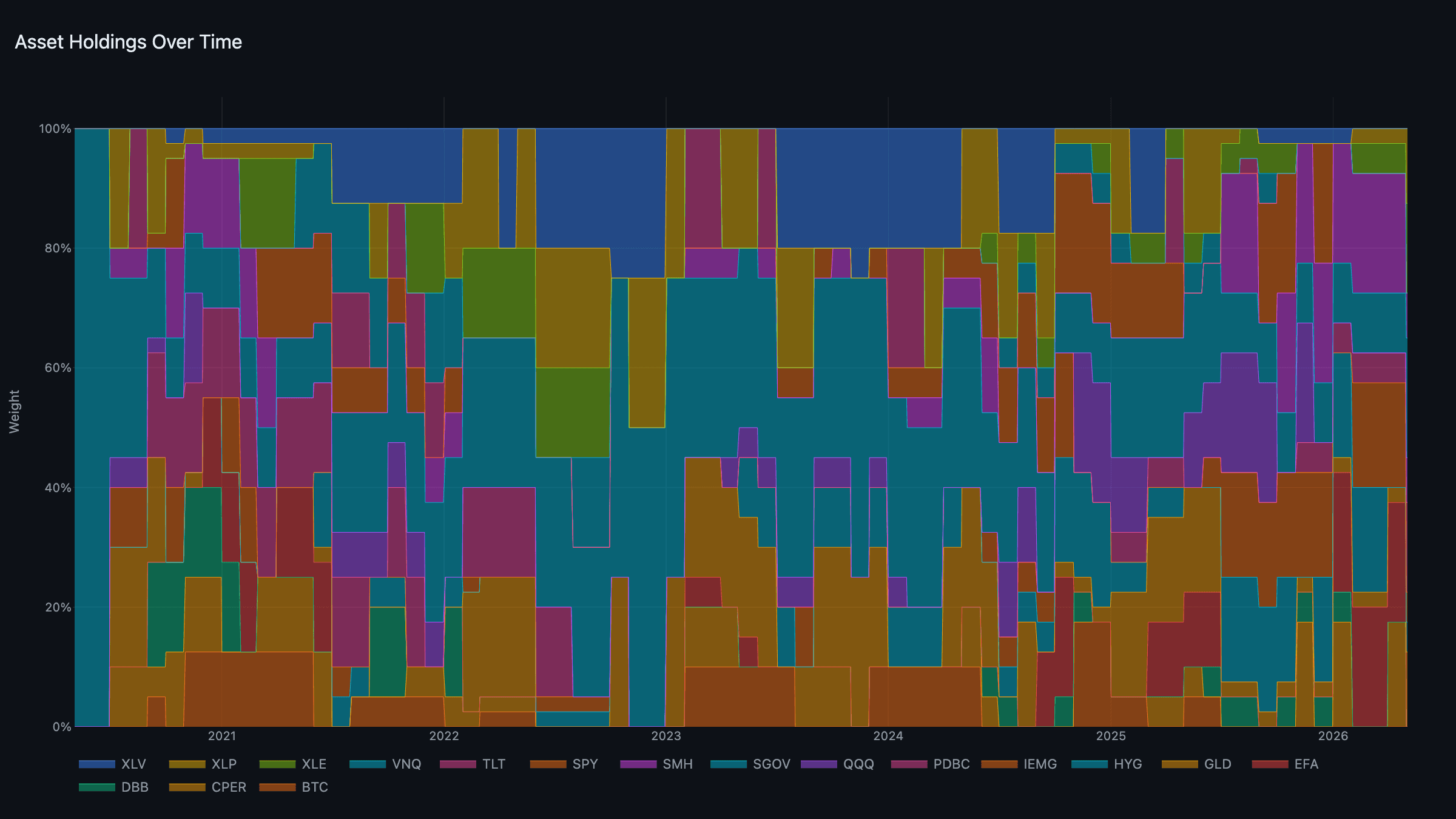

The Portfolio: Pivot to Real Assets

The regime change rewired the sleeve weights, and the tournament followed:

- Real assets (heaviest sleeve): PDBC + XLE — broad commodities and energy, the direct beneficiaries of the oil shock, at 15% each.

- Defensive: GLD + XLP — gold steps up as the inflation/uncertainty hedge, paired with staples, 12.5% each.

- Cash: SGOV at 20% — Reflation/Contracting carries a deliberately larger cash sleeve.

- Growth: SMH + QQQ — trimmed to ~7.5% each as the growth sleeve weight falls.

- Liquidity: IEMG + HYG — small positions.

This is the framework doing its job: the same energy spike that's a headwind for the consumer is a tailwind for the energy and commodity sleeves, and the model leaned into it without anyone making a discretionary call.

News: A Divided Fed Holds

The FOMC left the target range at 3.50%–3.75% Wednesday, but the headline was the split: 8–4, the most dissents in a single meeting since 1992. One member wanted a cut outright; three others backed the hold but refused to sign onto any easing bias. The statement flagged that elevated energy prices and "developments in the Middle East" are clouding the outlook.

That's a committee with no consensus, navigating an energy-driven inflation impulse it can't fix with rate policy — exactly the bind the debt-refinancing thesis anticipates. Separately, the Senate Banking Committee advanced Kevin Warsh's nomination for chair on party lines, setting up a full floor vote in the next two weeks.

Week Ahead

- Warsh floor vote: A full Senate confirmation could land within the fortnight; the succession is now the dominant Fed story.

- Labor data: The April jobs report will test whether the "solid activity, low job gains" picture the Fed described is holding.

- Oil: Still the master variable. Every Hormuz headline moves the inflation composite, and right now it's the swing factor between Reflation persisting and fading.

All model scores are normalized to a [-1, +1] scale through our proprietary normalization methodology. Positive readings indicate above-trend expansion; negative readings indicate below-trend contraction. Data updated through May 1, 2026.

MacroScope models are systematic tools, not investment advice. Past performance does not guarantee future results.