MacroScope Weekly — April 26, 2026

Current Regime: Goldilocks / Contracting Liquidity

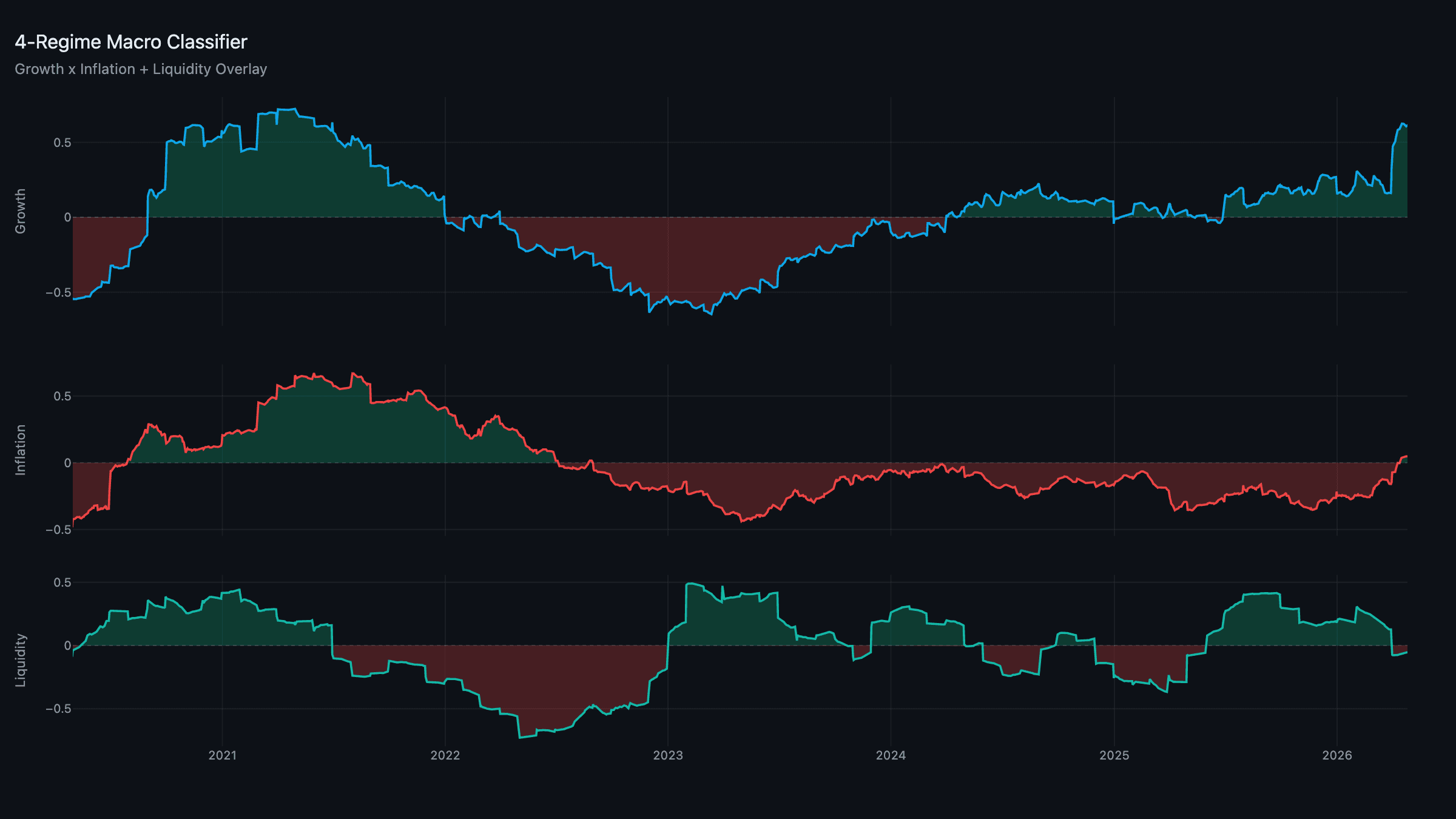

TL;DR: Growth is the strongest it has been all year — the composite sits near +0.6 on resilient production, capex, and a humming AI build-out — while the inflation composite is still hovering around zero, so the regime stays Goldilocks. The catch is liquidity: the composite has slipped negative, flipping the overlay to Contracting. That combination keeps the book risk-on but tightening the leash. Oil is the wildcard — Brent topped $108 this week as the latest round of US–Iran talks unravelled and the Strait of Hormuz stayed effectively shut. The Fed meets Tuesday–Wednesday.

Composites: Strong Growth, Draining Liquidity

Growth is carrying the framework. The composite is pinned near +0.6, with production and the decision/capex pillar both deep in positive territory — the data-center and semiconductor build-out is still the cleanest signal in the macro set. Inflation, despite the oil headlines, is only fractionally positive at the composite level: the energy spike is showing up in pipeline costs, but expectations and services are soft enough to keep the aggregate near the zero line.

The shift this week is liquidity, which has crossed below zero. Central-bank balance sheets are flat to shrinking, the dollar is firm, and the new collateral & funding pillar is reading mild stress as rate volatility stays elevated through the conflict. Positive growth with low inflation is still Goldilocks — but Contracting liquidity is the regime telling you to keep the risk on a shorter tether.

The Portfolio: Carrying a Risk-On Book

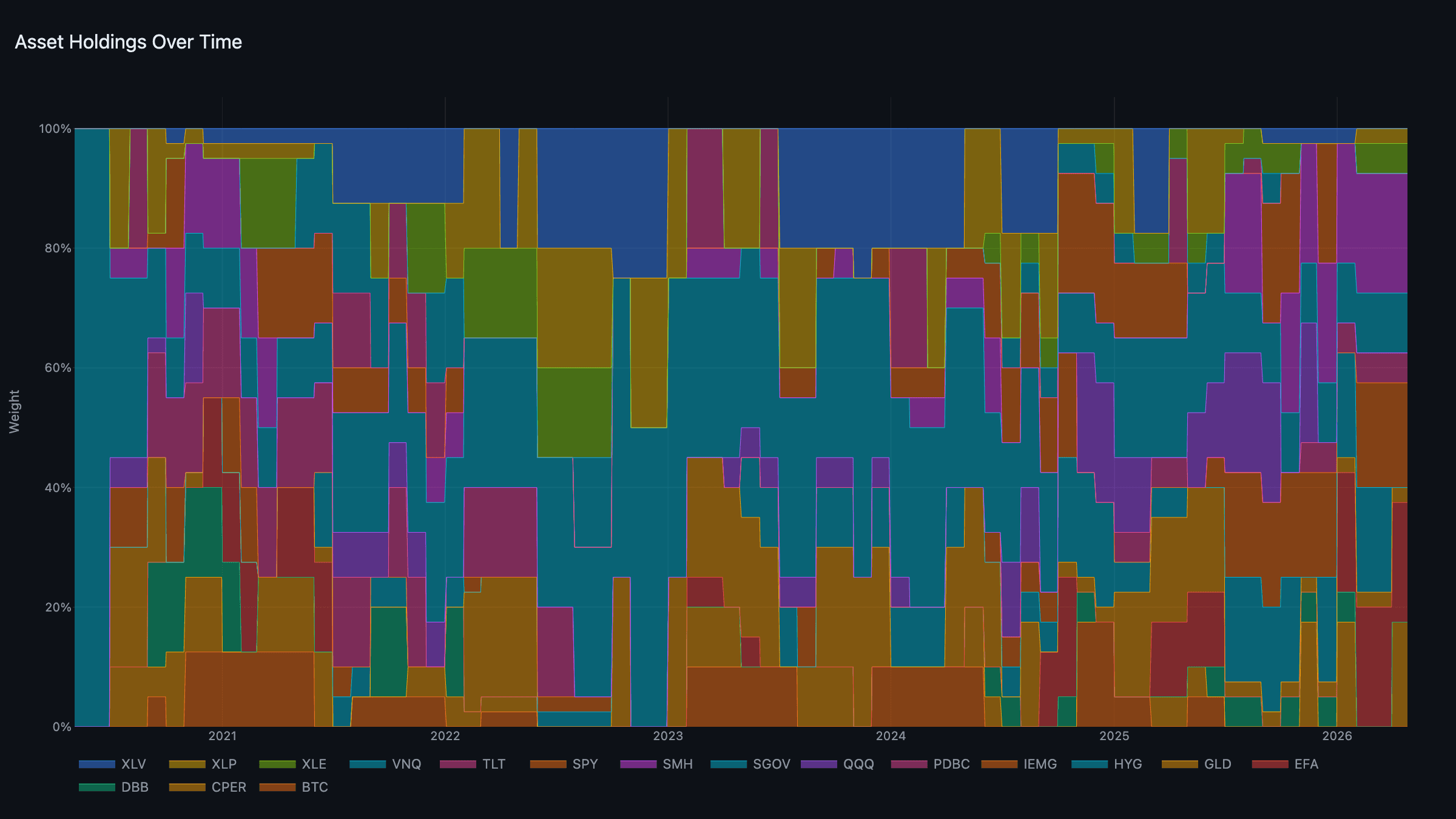

The book this week is still the risk-on allocation set at the start-of-April rebalance — when the prior read was Goldilocks with Expanding liquidity, so the growth and liquidity sleeves got the heaviest weights. The model rebalances monthly and holds between, so even though the overlay flipped to Contracting in early April, those weights are carried until the next month-start. The current book:

- Growth (heaviest): EFA + SMH — developed-ex-US equity and semiconductors, the two strongest names in the pool, ~20% each.

- Liquidity: IEMG + CPER — emerging markets and copper, riding the global-reflation and weak-dollar impulse, ~17.5% each.

- Real assets: XLE + PDBC — energy and broad commodities, the Hormuz-premium beneficiaries.

- Defensive: XLP + GLD — a small staples/gold ballast.

- Cash: SGOV at 10%.

The key forward point: if liquidity stays Contracting into the May rebalance, the sleeve weights re-cut more defensively — heavier defensive and cash, lighter growth. For now the model is carrying the risk-on book it built two weeks ago. Note too what the tournament isn't holding: US large-cap tech doesn't win the growth sleeve here — semis and ex-US do.

News: Oil Back to $108

The week's tape was about energy. Indirect US–Iran negotiations stalled again, and with the Strait of Hormuz still throttled — commercial crude traffic through the chokepoint remains down roughly 90% since the conflict began — Brent pushed back above $108. Each diplomatic headline is now worth several dollars a barrel in either direction, and this week the headlines went the wrong way.

Equities have been remarkably composed through all of it. The S&P is up low-single-digits on the year and has refused to break down on the oil spikes, which tells you the market is treating the energy shock as a tax rather than a recession trigger — for now. The longer Brent sits in triple digits, the harder that stance is to hold.

Week Ahead

- FOMC, Tuesday–Wednesday (Apr 28–29): No change expected, but the language on energy and the dot plot matter more than the decision. Watch the dissents — the committee is unusually split.

- Warsh committee vote: The Senate Banking Committee is expected to advance Kevin Warsh's nomination to chair alongside the meeting. The succession is now a live market variable.

- Liquidity: A continued drain would start to pressure the risk-on posture. The growth sleeve only earns its weight while the liquidity overlay doesn't deteriorate further.

All model scores are normalized to a [-1, +1] scale through our proprietary normalization methodology. Positive readings indicate above-trend expansion; negative readings indicate below-trend contraction. Data updated through April 24, 2026.

MacroScope models are systematic tools, not investment advice. Past performance does not guarantee future results.