MacroScope Weekly — April 19, 2026

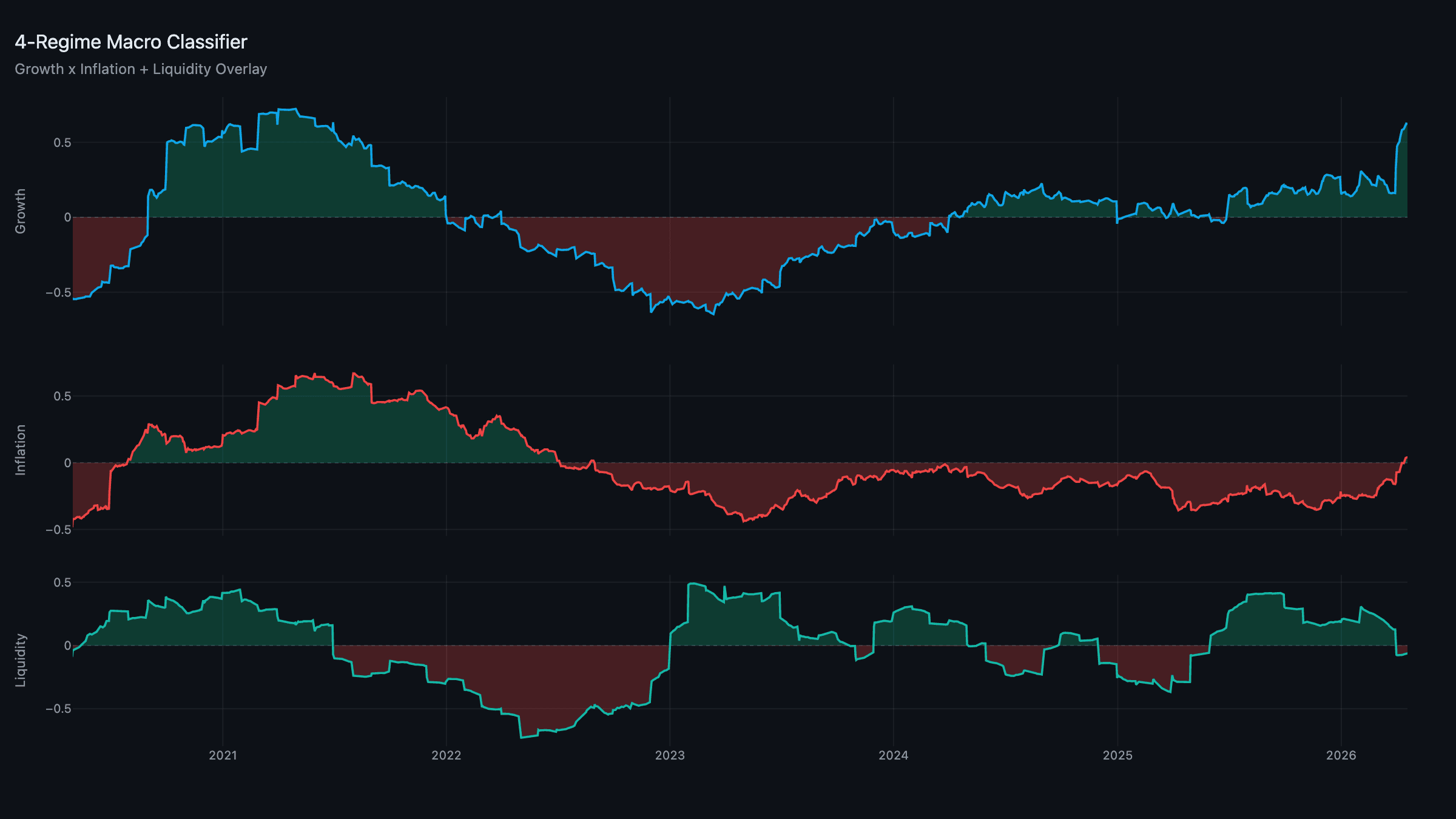

Current Regime: Goldilocks / Contracting Liquidity

TL;DR: Growth is the strongest it's been all cycle at +0.62, inflation is sitting right on the zero line, and liquidity is still mildly negative — so the regime holds at Goldilocks / Contracting. Markets have stopped reacting to the US–Iran headlines, the S&P has recovered off its lows, and crypto is quietly building a base. Fed net liquidity is draining this week, but that's the April tax-week pattern, not a policy signal. The book is still the risk-on allocation carried from the April rebalance, with the FOMC up next week.

Composites: Growth Leads, Liquidity Lags

Growth: +0.62 | Inflation: +0.04 | Liquidity: −0.06

Growth keeps powering higher — the capex and distribution pillars are firmly in control, and the soft factory data of March has faded into the background. Inflation has nudged just above zero (+0.04) but remains inside the hysteresis dead-band, so the classifier holds it on the Goldilocks side rather than flipping to Reflation on a borderline tick. Liquidity is the one negative leg at −0.06, keeping the overlay Contracting.

The shape of the regime is clear: a strong real economy with a tightening liquidity backstop. The whole question into May is whether liquidity turns — and part of this week's drain is mechanical, not structural.

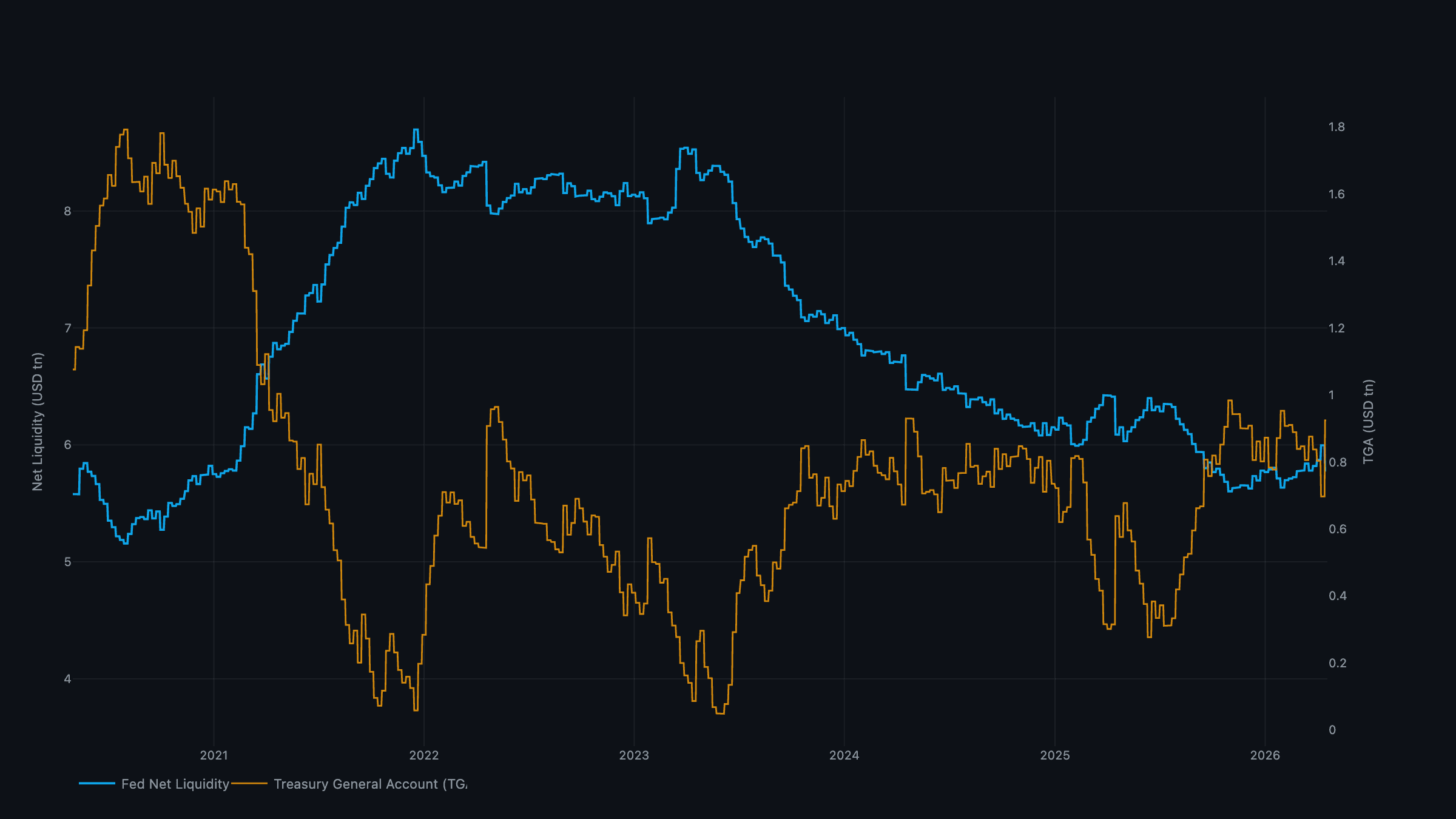

Liquidity: A Tax-Week Drain

Fed net liquidity has fallen meaningfully this week, which looks concerning against a regime that needs liquidity to turn — but it's largely the April tax-week pattern. Every year, the Treasury General Account balloons as tax payments flow in, mechanically pulling reserves out of the system. It's a calendar effect, not a policy shift, and it reverses as the Treasury spends back down in the following weeks.

Strip out the seasonal piece and the underlying liquidity picture is still soft but stabilising — private credit has stopped deteriorating and cross-border dollar flows are improving on a weaker dollar. If the post-tax-season bounce comes through in early-to-mid May, the overlay has a real shot at flipping to Expanding at the next rebalance. If it doesn't materialise by mid-May, that's when the drain stops being noise.

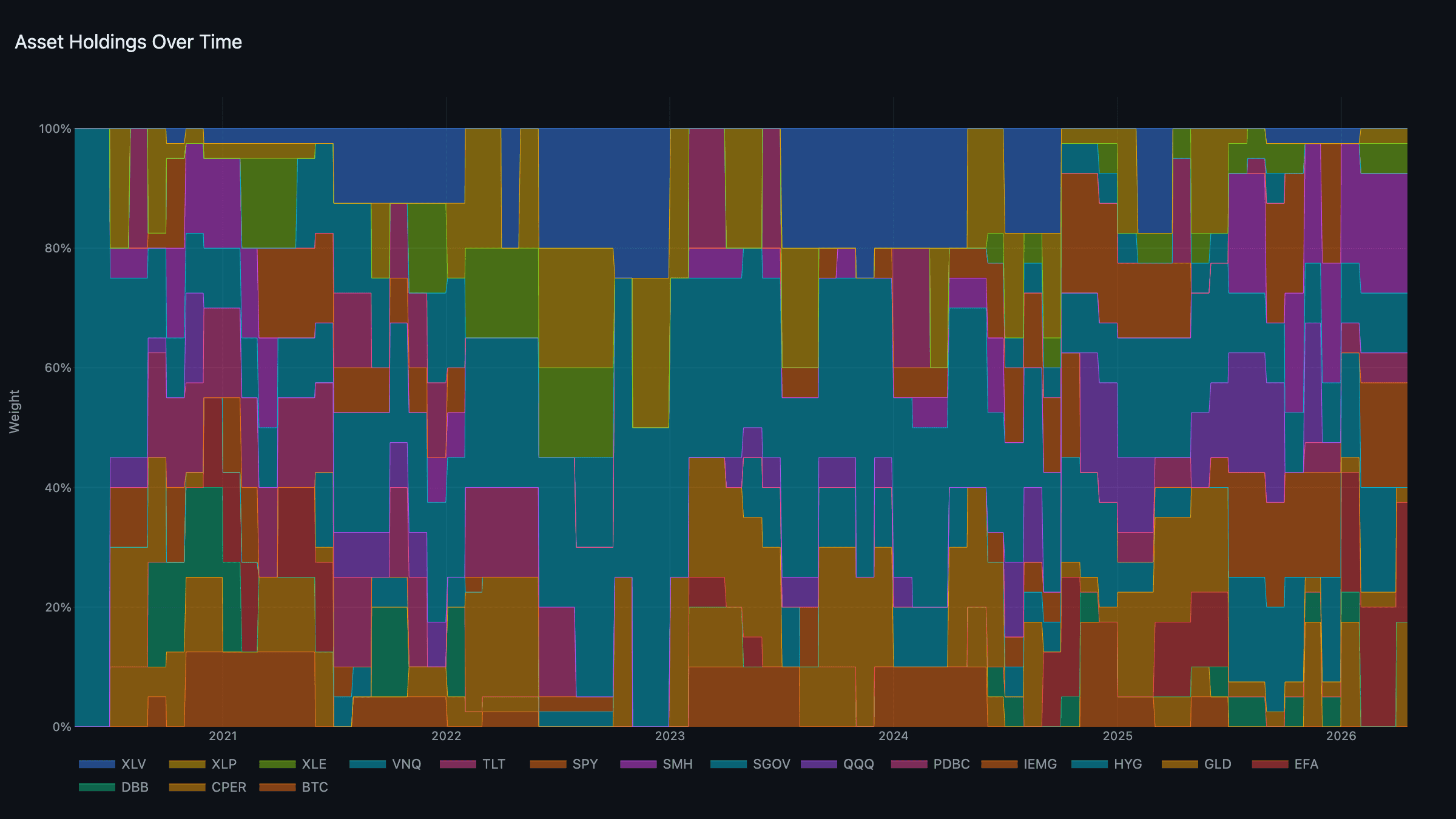

The Portfolio: Carrying Risk Into the FOMC

The book is still the risk-on allocation set at the April rebalance — growth and liquidity sleeves carrying the heaviest weights from the prior Expanding read:

- Growth (heaviest): EFA + SMH (~20% each).

- Liquidity: IEMG + CPER (~17.5% each).

- Real assets: XLE + PDBC.

- Defensive: XLP + GLD.

- Cash: SGOV, 10%.

The framework is positioned constructively into next week's Fed meeting and the month-end rebalance. If liquidity confirms a turn, the risk-on posture is reaffirmed; if the tax-week drain persists structurally, the May rebalance tilts more defensive. Either way the model acts mechanically at the rebalance rather than guessing now.

News: Markets Stop Reacting to the Middle East

The US–Iran situation dominated the tape for weeks; this week it largely dropped off it. Not because anything resolved — the ceasefire process is still rocky and oil is still bid — but because markets have stopped reacting. Oil is grinding sideways, equity vol is compressing, and credit spreads are calm. Markets ceasing to react to bad news, after the news has been in the tape long enough to be fully priced, is more often than not a constructive signal.

The S&P has staged a notable recovery off its recent lows with improving breadth — leadership has broadened beyond the megacaps into the ex-US, semiconductor, and EM names the tournament favours. Bitcoin and the broader crypto complex are doing the same thing more slowly: tighter ranges, fewer lows, the patient base-building that tends to precede a move. None of it is parabolic — and against a strong-growth backdrop with liquidity poised to potentially turn, that's the healthier setup.

Week Ahead

- FOMC (Apr 28–29): No change expected, but the language on energy and the dissents are what matter — the committee is unusually split.

- Warsh committee vote: The Senate Banking Committee is expected to advance Kevin Warsh's chair nomination; the succession is now a live market variable.

- Tax-week reversal: Watch for the post-tax-season liquidity bounce. Timing matters more than magnitude — it's the swing factor for whether the overlay flips Expanding at the May rebalance.

All model scores are normalized to a [-1, +1] scale through our proprietary normalization methodology. Positive readings indicate above-trend expansion; negative readings indicate below-trend contraction. Data updated through April 17, 2026.

MacroScope models are systematic tools, not investment advice. Past performance does not guarantee future results.