MacroScope Weekly — April 12, 2026

Current Regime: Goldilocks / Contracting Liquidity

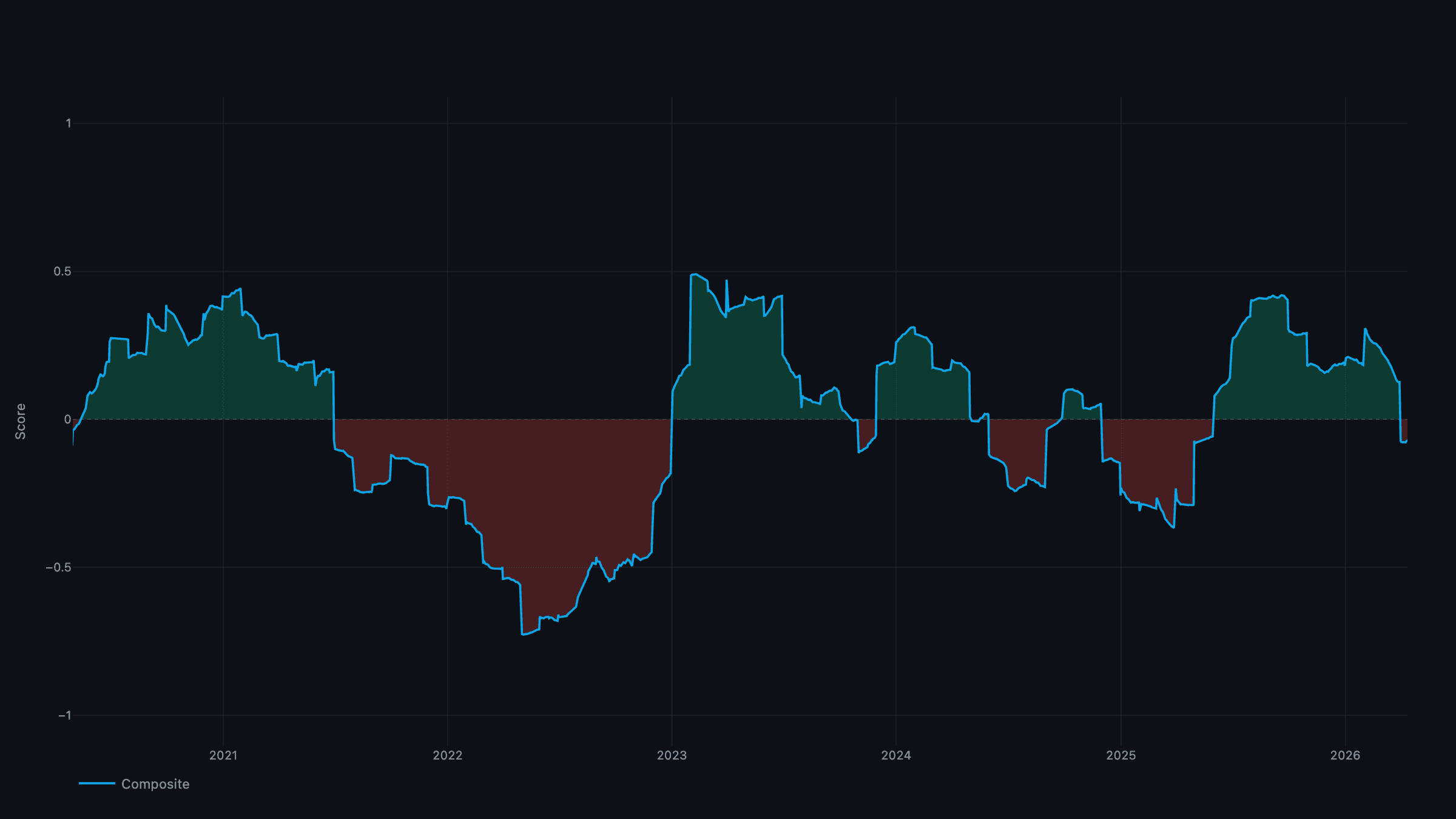

TL;DR: Growth keeps strengthening — the composite is up to +0.58 — while inflation sits right on the zero line and liquidity remains negative. That keeps us in Goldilocks / Contracting: a strong real economy with a tightening liquidity backstop. The book is still the risk-on allocation carried from the April rebalance. The US–Iran conflict dominates the tape, but markets have largely priced the tail risk and the reflationary undertone persists.

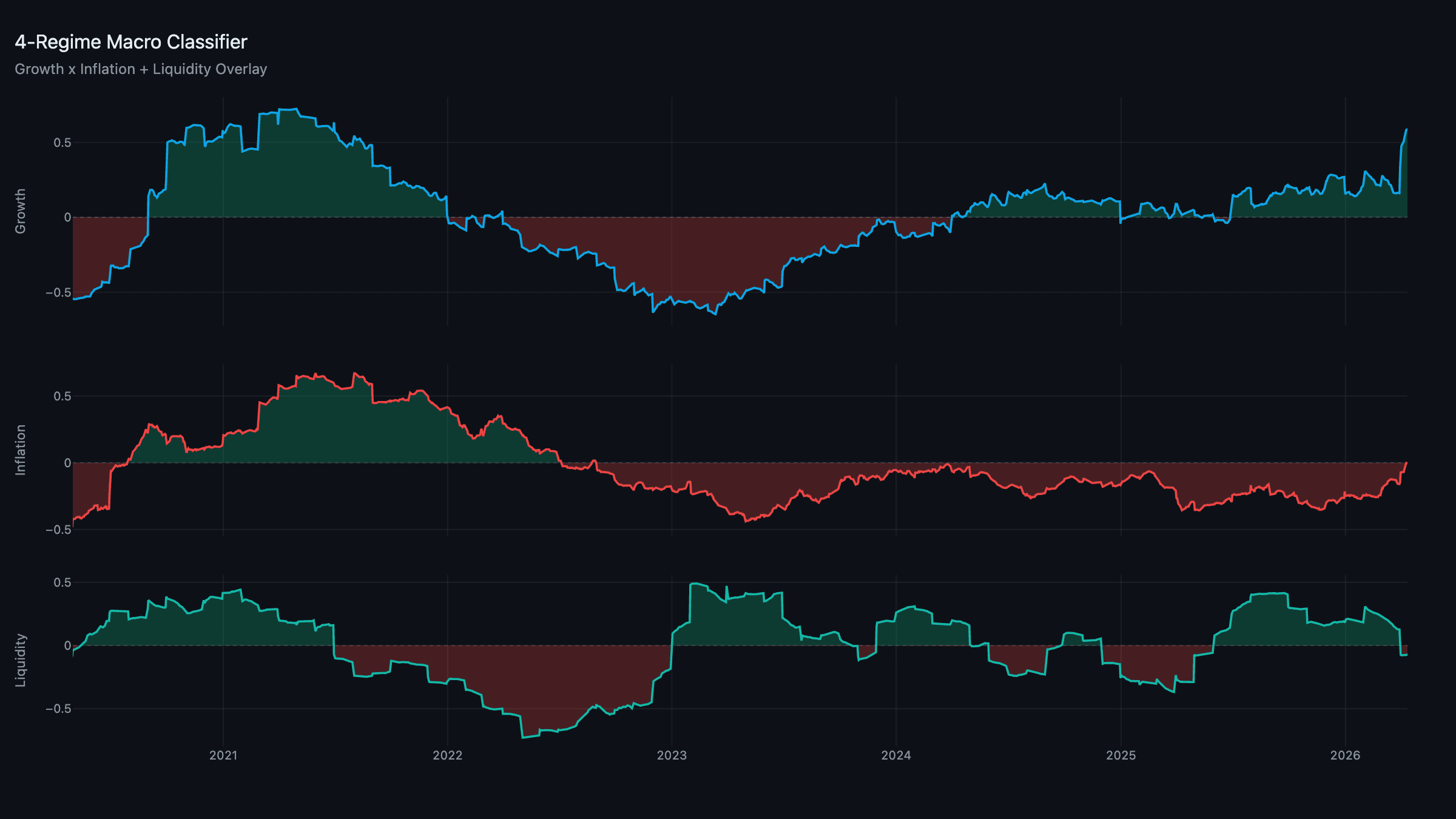

The Regime: Strong Growth, Inflation at the Line

Growth: +0.58 | Inflation: −0.00 | Liquidity: −0.07

Growth is the standout — its strongest reading in months and still climbing, driven by the capex and distribution pillars even as the cyclical factory data stays soft. Inflation is balanced precisely at zero: the energy-and-tariff impulse is pushing the pipeline channel up, but disinflationary services and demand are pulling against it, leaving the aggregate at the threshold. Liquidity is still negative, so the overlay holds at Contracting.

The honest read: inflation is one decisive tick from flipping the regime to Reflation, and liquidity is one tick from flipping the overlay to Expanding. We're sitting on two thresholds at once — which is exactly when the hysteresis dead-band earns its keep, holding the regime steady until a move is real.

Growth & Inflation: Firm and Balanced

Growth at +0.58 continues to defy the soft cyclical headlines. The leading pillars — corporate capex on the AI build-out, distribution on resilient freight and cloud — are carrying the composite, and the deceleration narrative that dominated March has stalled. The economy is firmer than the manufacturing surveys suggest.

Inflation at −0.00 is the balance point. March CPI, released midweek, landed near consensus — enough to keep the pipeline-costs and expectations channels firm, not enough to overpower the disinflationary services side. The tariff and energy impulses are still the upside risk; a hot print or a fresh oil spike is what tips the composite positive and the regime into Reflation.

Liquidity: Still the Constraint

Liquidity holds at −0.07. Private credit and the funding pillars haven't yet turned, and central banks remain frozen by the inflation backdrop. This is the variable that separates "growth that shows up in asset prices" from "growth trapped in the real economy" — and right now it's the lone leg keeping the framework from a fully risk-on green light.

In a debt-refinancing economy, something eventually has to give on the liquidity side to keep the system funded. When that adjustment comes, the liquidity composite is the first place it shows — and a flip to Expanding would be the most constructive development available. It hasn't happened yet.

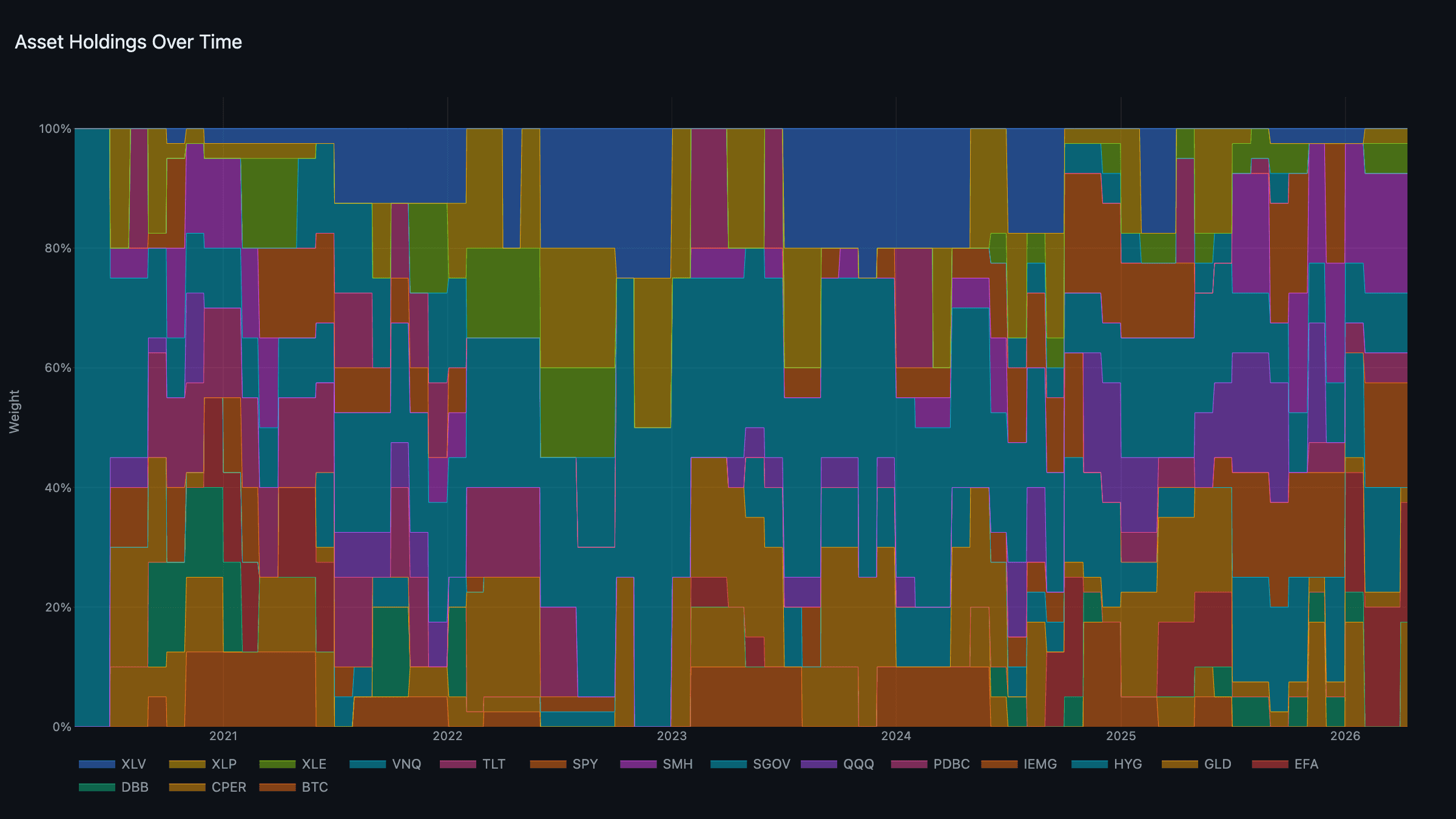

The Portfolio: Carrying the Risk-On Book

Unchanged from last week — the allocation set at the April 1 rebalance, when the prior read was Goldilocks/Expanding, carried by the monthly cadence:

- Growth (heaviest): EFA + SMH (~20% each).

- Liquidity: IEMG + CPER (~17.5% each).

- Real assets: XLE + PDBC.

- Defensive: XLP + GLD.

- Cash: SGOV, 10%.

With liquidity still Contracting, the May rebalance is the next decision point — if it persists, the weights tilt defensive; if it flips Expanding, the risk-on posture is reaffirmed and likely extended. For now the model is carrying measured risk across five sleeves, with gold a small holding rather than the anchor.

The Other Story: US–Iran

The geopolitical headline still dominating the tape is the US–Iran confrontation. Talks are on-again-off-again, military posture is elevated, and the ground situation remains ambiguous.

What the market appears to be saying: the risk is largely priced. Oil spiked on the initial escalation and has settled into a range; equities wobbled but haven't broken; credit spreads widened modestly and retraced. The classic war-premium trades — long oil, long defense, short equities — haven't sustained, which usually means positioning already reflects the tail risk. Combine that with a strengthening growth composite and the path of least resistance stays constructive — unless a genuine, sustained supply-lane disruption forces a re-rating. The portfolio doesn't need a view on the geopolitics; it follows the regime and the tournament.

Week Ahead

- Regime thresholds: Watch inflation and liquidity — both are sitting on their dead-band edges. A move in either flips the regime, and the May rebalance will act on whatever sticks.

- Retail sales / data: Confirmation of whether the consumer is still spending through the confidence slump.

- US–Iran headlines: Still the swing factor for oil, and therefore for the inflation composite.

All model scores are normalized to a [-1, +1] scale through our proprietary normalization methodology. Positive readings indicate above-trend expansion; negative readings indicate below-trend contraction. Data updated through April 10, 2026.

MacroScope models are systematic tools, not investment advice. Past performance does not guarantee future results.