MacroScope Weekly — April 5, 2026

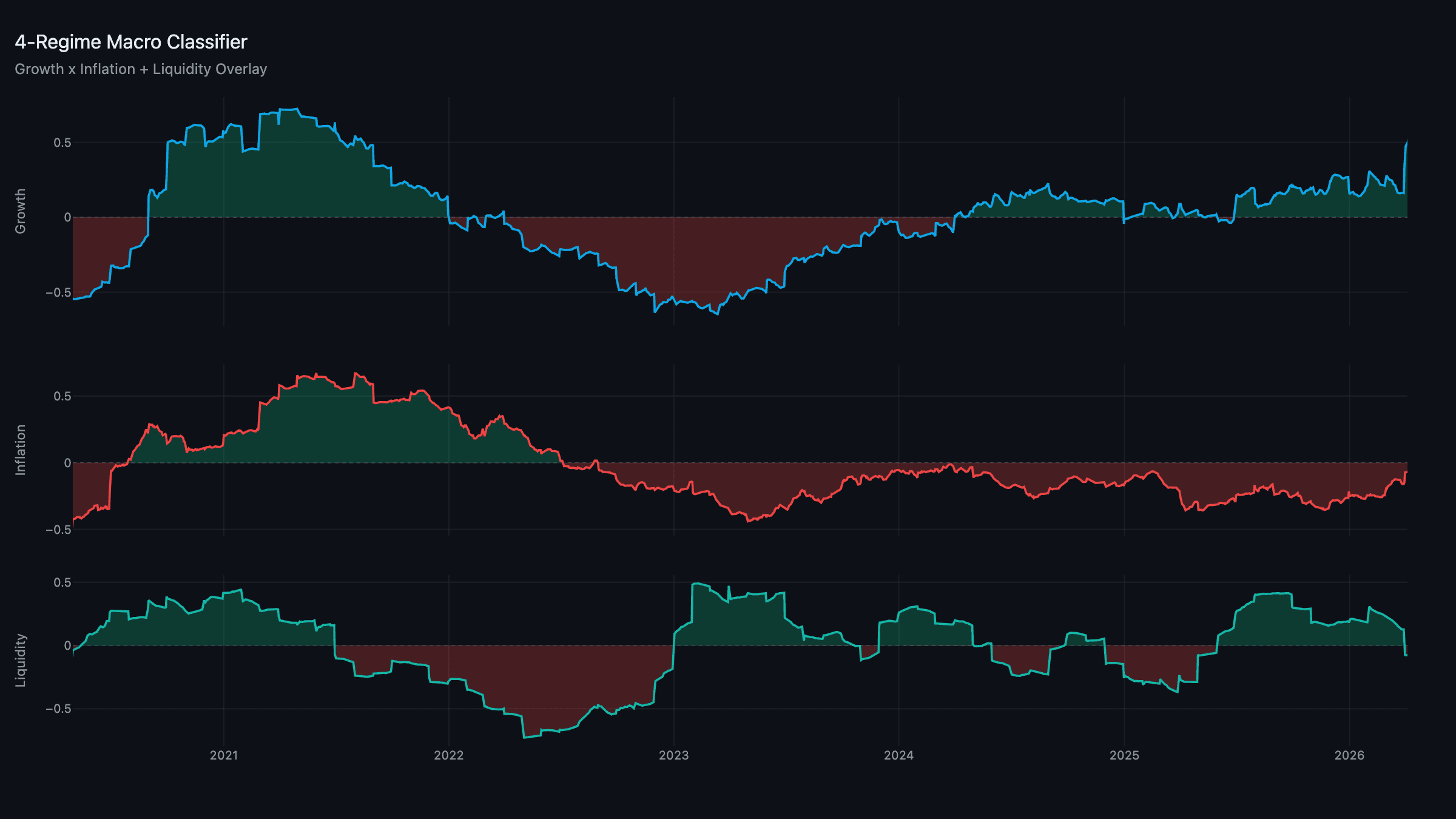

Current Regime: Goldilocks / Contracting Liquidity

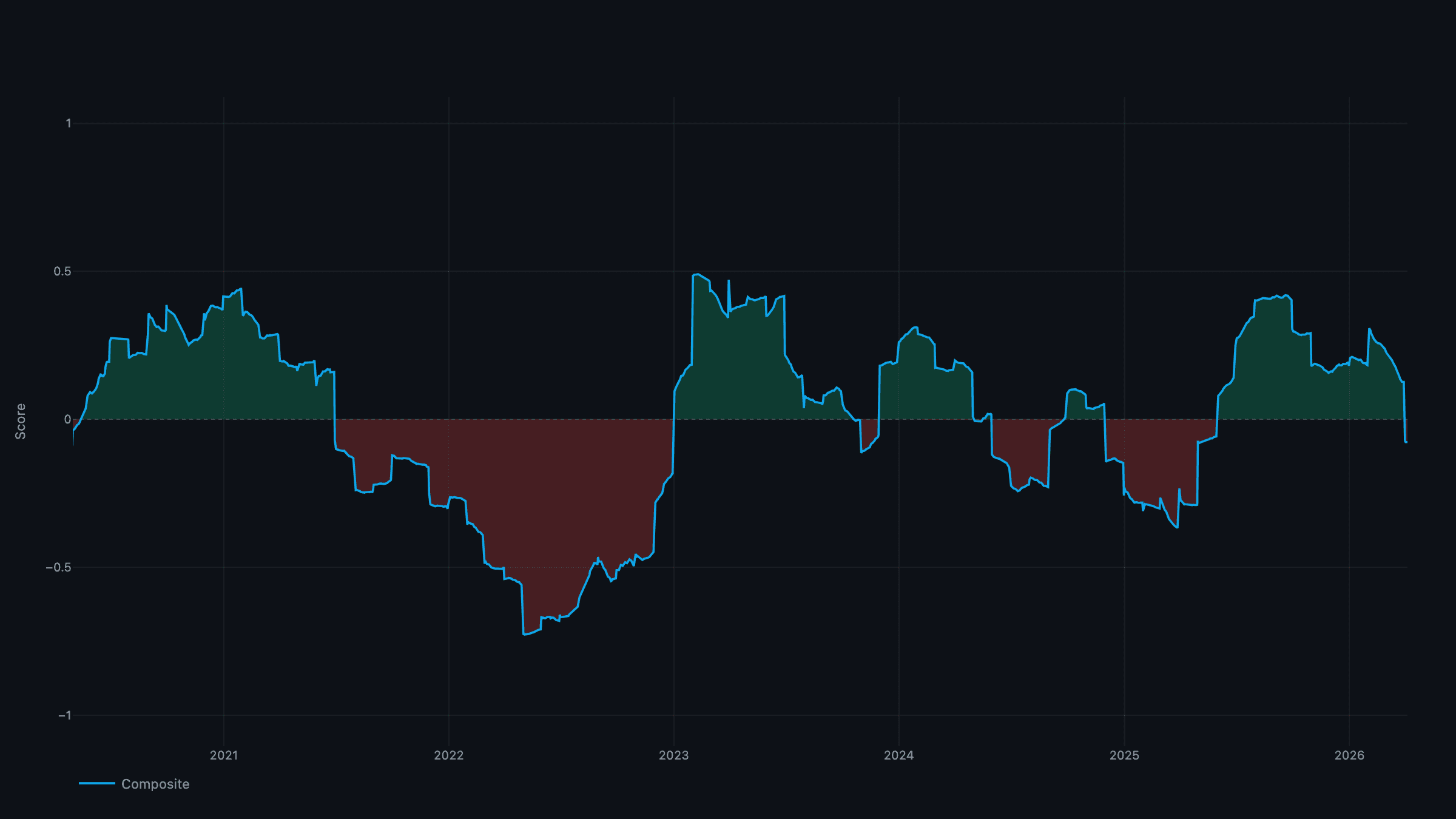

TL;DR: The overlay flipped. Growth is actually firming — the composite jumped to +0.48 as the capex and distribution pillars more than offset a soft factory sector — and inflation is still negative, so the regime stays Goldilocks. But liquidity crossed below zero this week, turning the overlay to Contracting. The book is still the risk-on allocation set at the April 1 rebalance; the defensive re-weight, if liquidity stays soft, comes at the next month-start.

The Regime: Goldilocks, Now Contracting

Growth: +0.48 | Inflation: −0.07 | Liquidity: −0.08

Two things stand out. First, growth is stronger than the headlines suggest — the composite is at its best level in months, carried by the AI capex cycle and resilient distribution even as manufacturing stays soft. Second, liquidity has flipped negative, moving the overlay from Expanding to Contracting. Inflation is still below trend, so the quadrant remains Goldilocks — but Contracting liquidity is the regime putting a speed limit on risk.

Growth: Soft Factory, Firm Composite

The cyclical data is genuinely weak: March payrolls printed just +38K, unemployment ticked to 4.5%, and ISM manufacturing held at 48.1 in contraction. Korean exports — a global-trade bellwether — slowed a second month, and high-yield spreads widened to ~420bps. On the surface, that reads as a fading economy.

But the growth composite is at +0.48 and rising, because the pillars that lead the cycle are strong: corporate capex (the AI build-out is relentless) and the distribution pillar (freight plus hyperscaler cloud) are carrying the signal while production lags. The framework weights the leading and coincident pillars together, and right now the leaders are winning. The watch item is whether the factory weakness eventually drags the leaders down — but it hasn't yet.

Inflation: Broadening Upstream, Still Below Trend

The inflation picture is firming at the edges. Pipeline costs keep grinding higher — March PPI showed broad-based gains across metals, chemicals, and food inputs, no longer just energy — and the University of Michigan's 5-year inflation expectations jumped to 3.3%, the highest since 2022. Oil eased to ~$97 on a partial Red Sea de-escalation, but the EU steel/aluminum tariffs due April 15 add a fresh imported-inflation impulse.

Still, the composite reads −0.07 — below trend. Services inflation remains disinflationary (shelter has stopped falling but isn't rising), and demand-pull pressure is only marginally positive. The energy-and-tariff impulse is real but hasn't broadened enough to flip the aggregate. This is precisely the supply-driven inflation the debt-refinancing thesis anticipates — the cost of keeping financial conditions loose enough to roll the debt.

Liquidity: The Overlay Turns

Liquidity fell to −0.08, the trigger for this week's overlay flip. Private credit is the drag — commercial and industrial loans have declined for a third straight month and small-business credit availability is at multi-year lows. Central banks are on hold with no easing in sight given the inflation trajectory, and only cross-border dollar flows remain marginally positive.

This is the tension at the core of the environment: the Treasury needs manageable refinancing rates, the economy needs lower rates, but inflation keeps the Fed frozen. Something gives eventually — and the liquidity composite will be the first place it shows up.

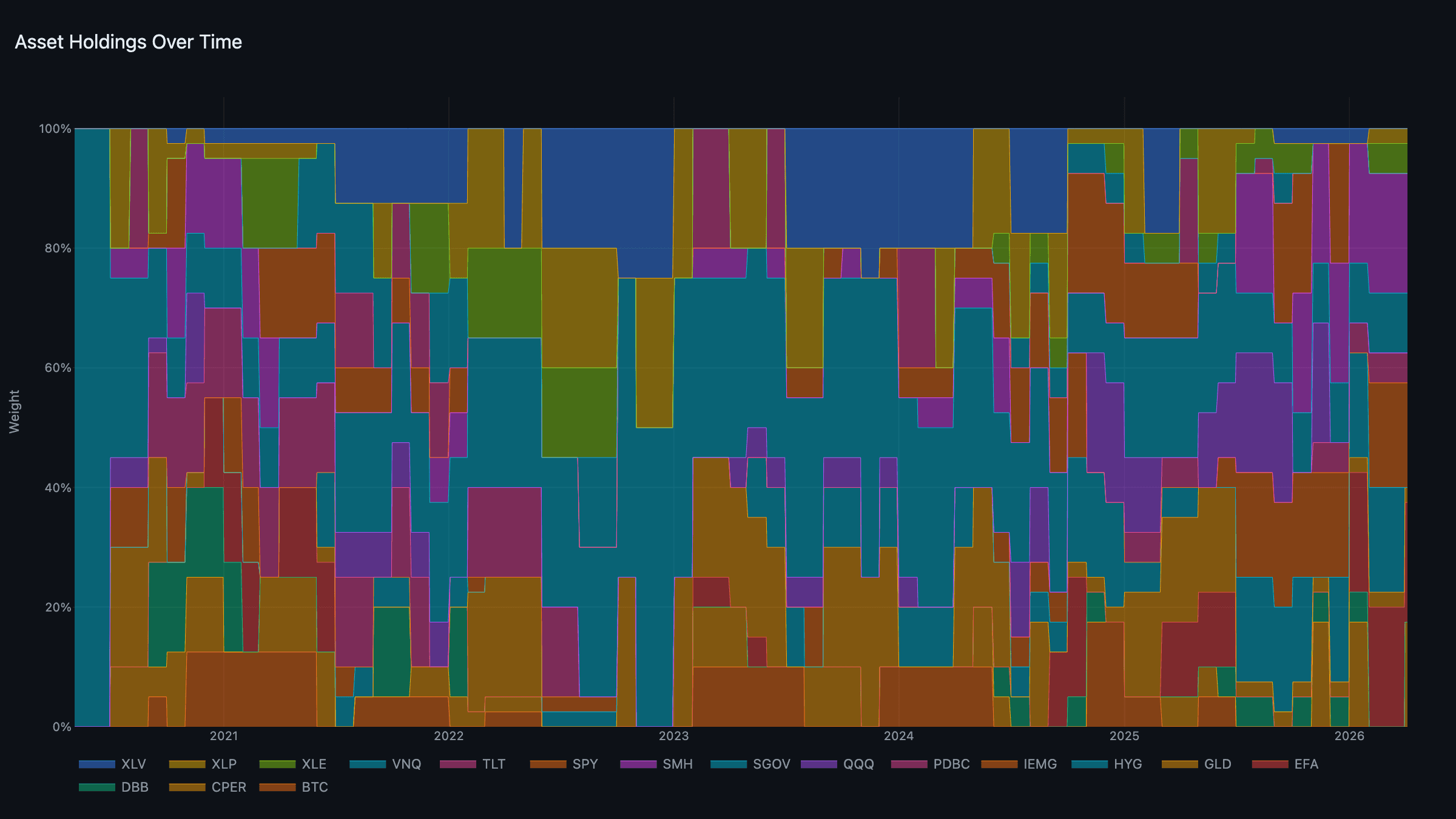

The Portfolio: Carrying the Risk-On Book

The book is the allocation set at the April 1 rebalance, when the prior read was still Goldilocks/Expanding — so growth and liquidity got the heaviest weights, and the monthly cadence carries them until the next rebalance:

- Growth (heaviest): EFA + SMH (~20% each).

- Liquidity: IEMG + CPER — copper edged out high-yield this month on stronger momentum (~17.5% each).

- Real assets: XLE + PDBC — the Reflation-style beneficiaries.

- Defensive: XLP + GLD — light ballast.

- Cash: SGOV, 10%.

The forward point: with liquidity now Contracting, the May rebalance will tilt the weights toward defensive and cash if it persists. Gold at $5,310 (+12% YTD) is in the book only as a small defensive holding — in Goldilocks it doesn't win a heavy weight, regardless of its strong year. The S&P at 6,350 and bitcoin at $76,800 sit behind the ex-US, EM, and semiconductor names the tournament prefers.

Week Ahead: Tariffs Take Effect

- ISM Services (Apr 7): The services sector is the economy's backbone — a sub-50 print would be a real negative for the growth composite.

- March CPI (Apr 10): Core consensus +0.3% MoM. An upside surprise reinforces the upstream inflation trend and pushes the Fed further from any cut.

- EU tariffs effective (Apr 15): First tariff expansion beyond China; a direct input to the pipeline-costs channel and a retaliation risk.

- Retail Sales (Apr 16): Spending has held up despite weak confidence — actual retrenchment would weigh on growth.

All model scores are normalized to a [-1, +1] scale through our proprietary normalization methodology. Positive readings indicate above-trend expansion; negative readings indicate below-trend contraction. Data updated through April 3, 2026.

MacroScope models are systematic tools, not investment advice. Past performance does not guarantee future results.