MacroScope Weekly — March 29, 2026

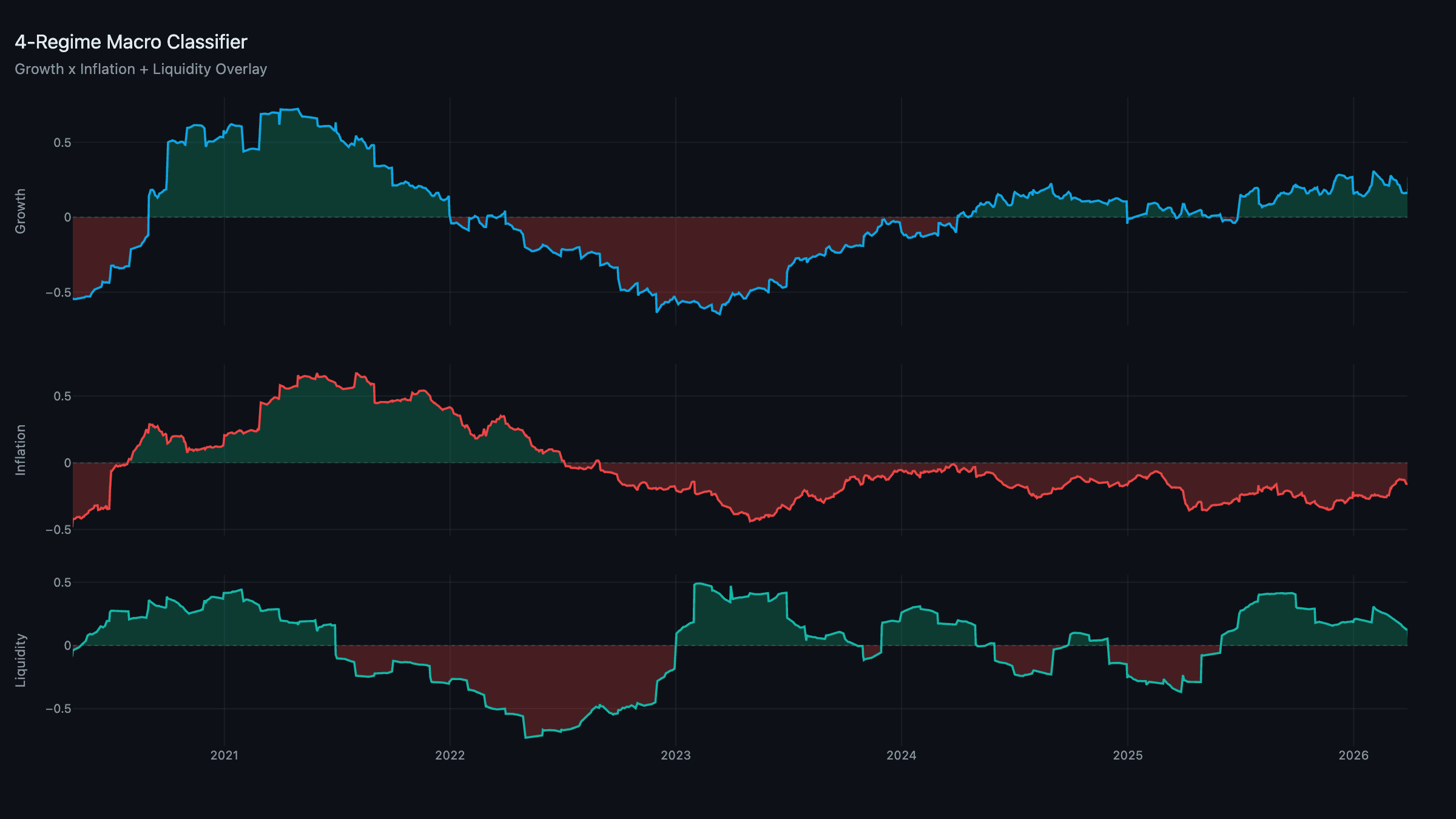

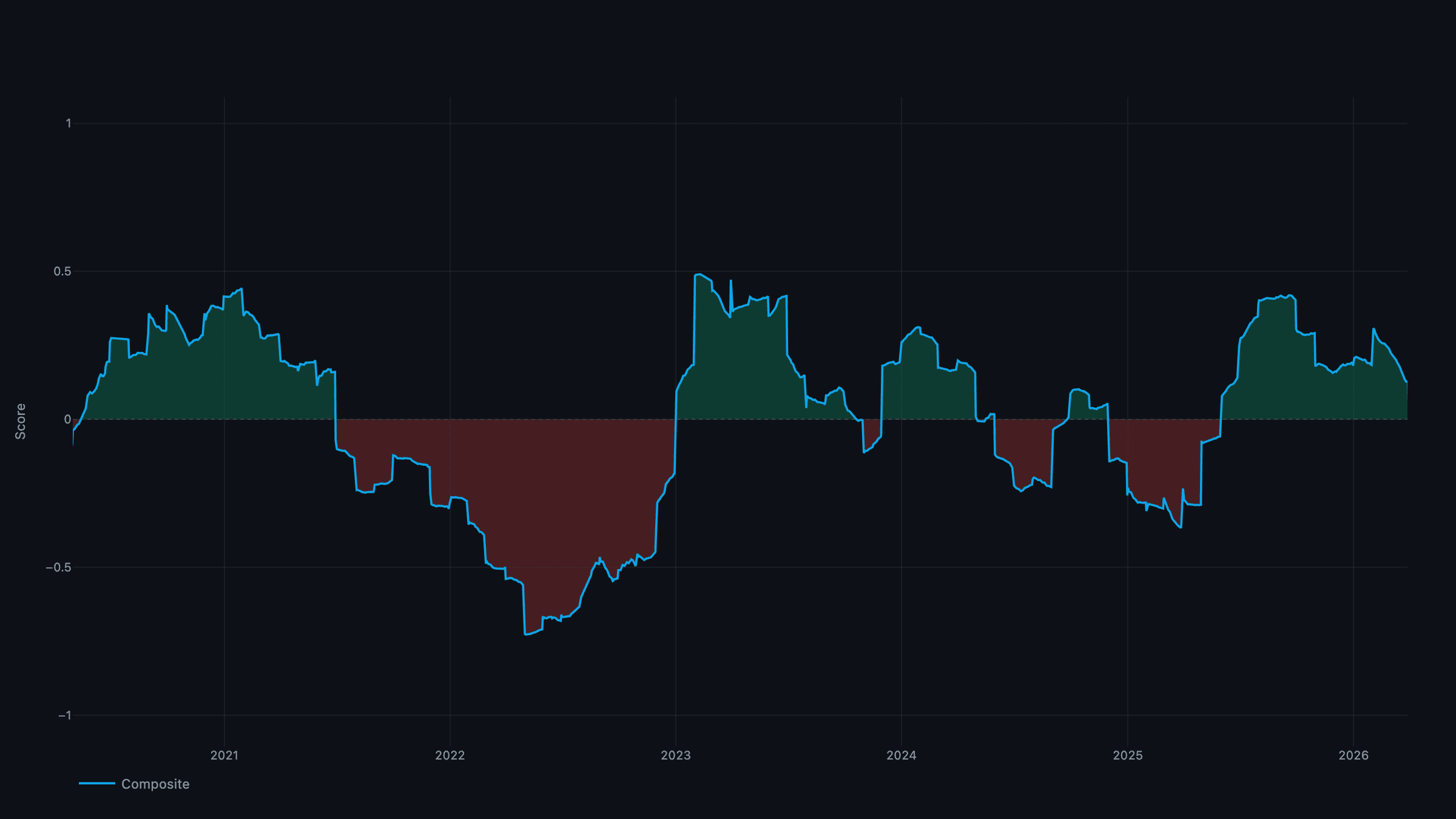

Current Regime: Goldilocks / Expanding Liquidity

TL;DR: Fourth straight week of Goldilocks / Expanding. Growth is softening at the margin but holding positive, the inflation composite is still negative as the energy shock stays narrow, and liquidity is expanding. The hard data is mixed — ISM manufacturing slipped back into contraction and core PCE ran a touch hot — but neither is enough to flip the regime. The book stays risk-on and globally tilted.

The Regime: Goldilocks Holds

Growth: +0.16 | Inflation: −0.16 | Liquidity: +0.13

No regime change, and the composition is stable: modest-but-positive growth, sub-zero inflation, expanding liquidity. The subtle trend is a slow divergence — growth grinding lower while pipeline inflation firms — but both are well short of the thresholds that would tip this toward Reflation or Stagflation. For now it's the same constructive backdrop that's held for a month.

Growth: Holding, But Narrowing

Growth at +0.16 is positive on a narrowing base. Production is the concern: the March flash showed industrial production down 0.2%, and ISM manufacturing printed 48.4, back in contraction after two months above 50. The manufacturing soft patch the February jobs data hinted at is now in the hard data.

What's holding the composite up is the same front-of-pipeline strength: corporate capex (AI build-out) and the distribution pillar (robust freight plus hyperscaler cloud) are providing a floor while the cyclical pillars soften. Financial conditions are marginally tighter — 10-year near 4.42%, high-yield spreads a touch wider — but the curve is still positively sloped. Section 301 escalation is now confirmed, with new duties on EU steel and aluminum slated for April 15, a forward headwind for the input pillar.

Inflation: Firming Upstream, Still Negative Overall

Core PCE came in at +0.35% MoM (2.9% YoY), a touch above consensus, and pipeline costs hit their highest since late 2025 as the oil-to-goods transmission accelerates. So the upstream pressure is real and building.

And yet the composite reads −0.16. The reason is unchanged: services inflation, while no longer falling quickly, is still disinflationary, and demand-pull pressure is negative. The inflation impulse is concentrated in a narrow energy/goods channel — which keeps the aggregate below trend and the regime in Goldilocks. The watch item is the same as last week: if services stabilizes while energy and goods keep climbing, the composite grinds toward the line.

Liquidity: Expanding

Liquidity holds at +0.13. Balance sheets and cross-border dollar funding are supportive, the dollar remains soft (DXY ~99.2), and the collateral/funding pillar is calm. This is the leg that lets the book stay risk-on through a manufacturing soft patch — expanding liquidity is the fuel, and it's still flowing.

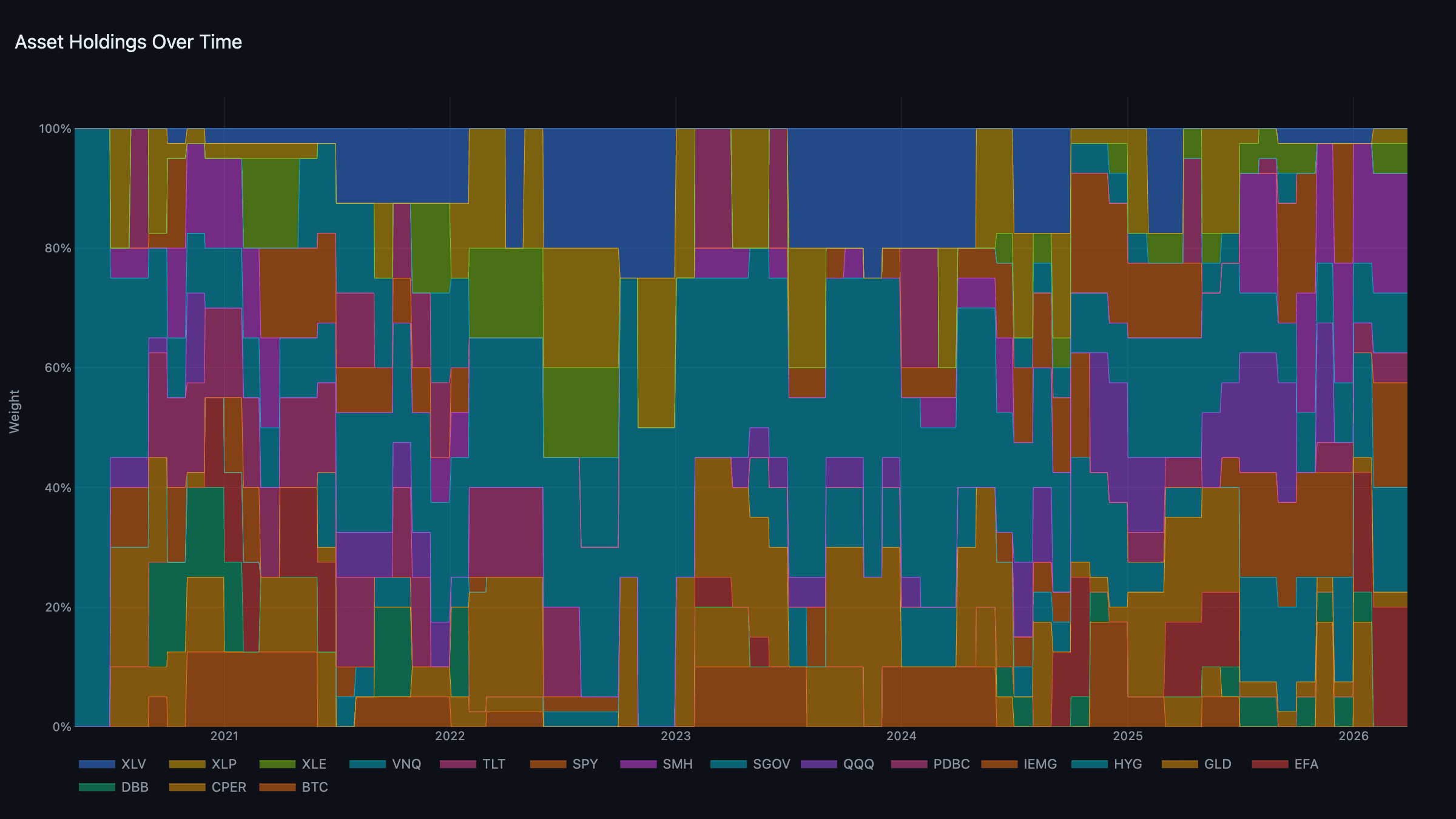

The Portfolio: Still Risk-On

No regime change means the book is unchanged — the risk-on Goldilocks/Expanding allocation:

- Growth: EFA + SMH (~20% each).

- Liquidity: IEMG + HYG (~17.5% each).

- Real assets: XLE + PDBC — the supply-side inflation beneficiaries.

- Defensive: XLP + GLD — light ballast.

- Cash: SGOV, 10%.

Gold at $5,240 had a volatile week of profit-taking, but it remains a small defensive holding regardless — the model holds the strongest names in each sleeve, and in Goldilocks gold simply doesn't win a large weight. Commodities and energy continue to earn their real-assets slots on the oil bid. The discipline here is not a flight to cash; it's holding measured risk across five sleeves while the constructive regime persists.

Week Ahead: Jobs and Tariffs

- ISM Manufacturing (Apr 1): Another sub-50 print would confirm the manufacturing contraction is deepening; watch prices-paid for pipeline pressure.

- March Nonfarm Payrolls (Apr 4): After February's −92K shock, consensus is a modest rebound to ~+45K. Another negative print would accelerate the growth slide and raise Stagflation risk.

- EU tariff effective date (Apr 15): New steel/aluminum duties feed the pipeline-costs channel.

- Oil: Brent's pullback toward $99 is encouraging; any Red Sea de-escalation is the most impactful catalyst for the inflation composite.

All model scores are normalized to a [-1, +1] scale through our proprietary normalization methodology. Positive readings indicate above-trend expansion; negative readings indicate below-trend contraction. Data updated through March 27, 2026.

MacroScope models are systematic tools, not investment advice. Past performance does not guarantee future results.